Estimated reading time: 13 minutes

The European Union (EU) potato harvest saw mixed results. The Dutch potato crop reached 3.598 million tonnes, marking a 6.5% increase over the previous year due to higher yields and expanded area, despite a reduced starch area. Belgium’s crop is only 2.5% larger, at 4.550 million tonnes, with yields down 3.1%, leading to expected imports. Most harvests are now complete, and dry weather is expected to aid the remaining progress. Prices are steady, with April 2025 futures at €288/tonne.

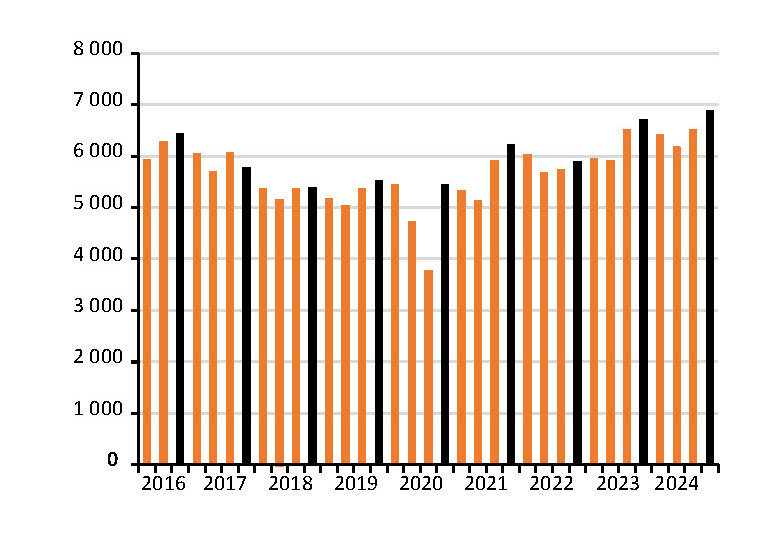

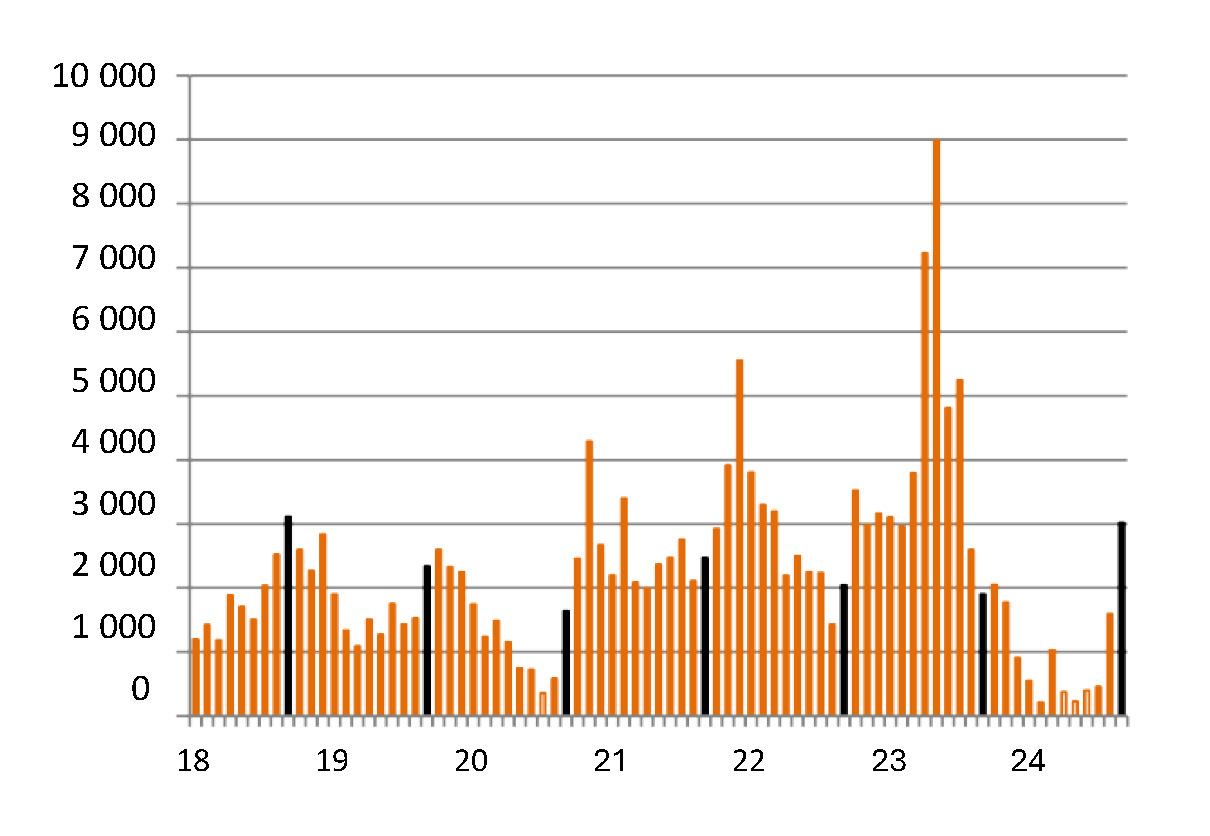

Meanwhile, McDonald’s saw record sales, though demand for fries fell in the Gulf, while Japan sales rose in September.

Quick service restaurants

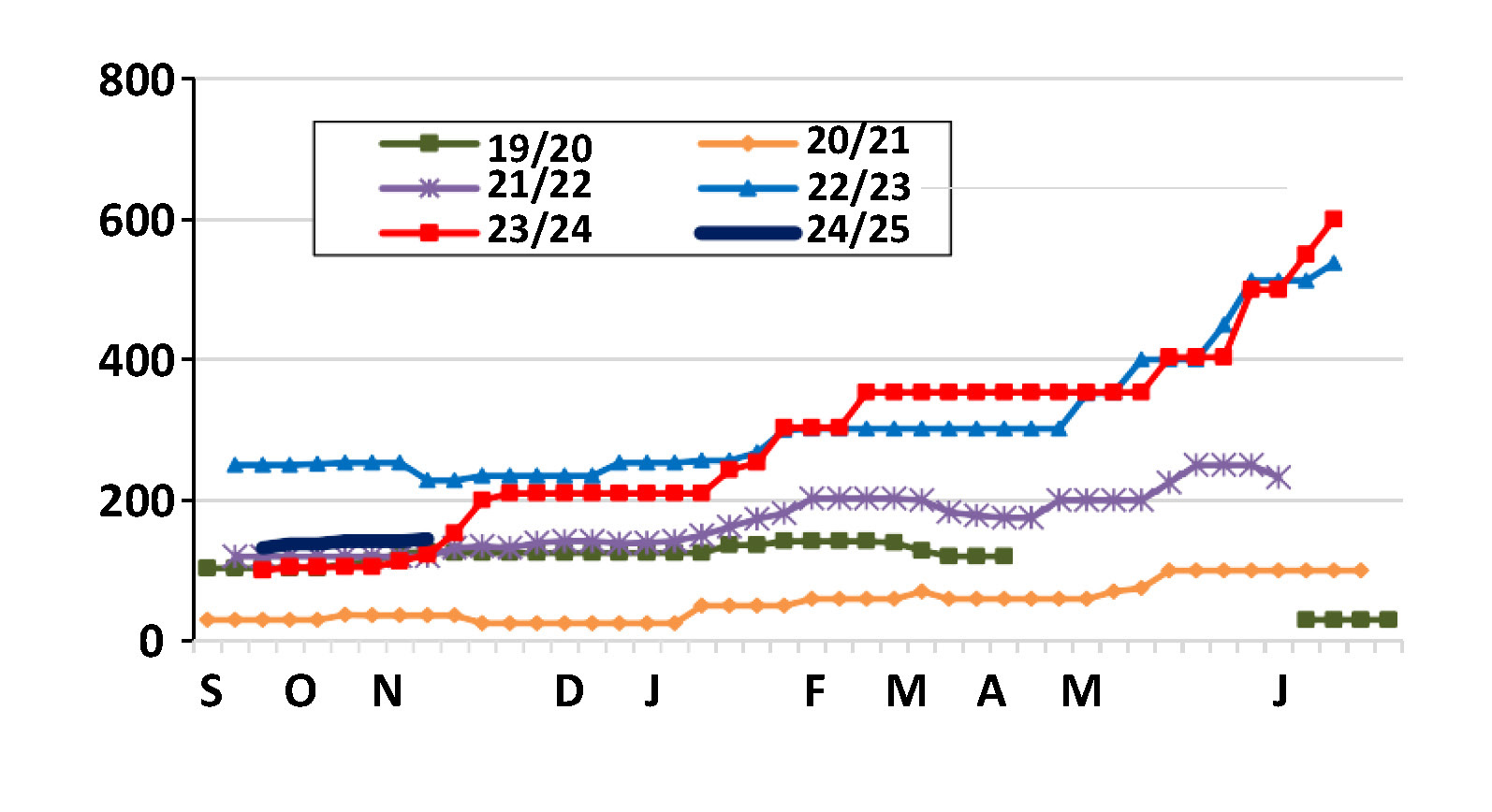

McDonald’s share price peaked at US$316 on 18 October 2024 before declining to US$295 by late October.

The brand surfaced in the United States (US) presidential campaign. Key election topics included farm policy, labour issues, and trade.

Trump proposed cutting energy costs, increasing farm support, and raising tariffs by 60% on Chinese imports and 10% on others.

Figure 1: McDonald’s quarterly sales in US$ millions.

Japan fry imports surge

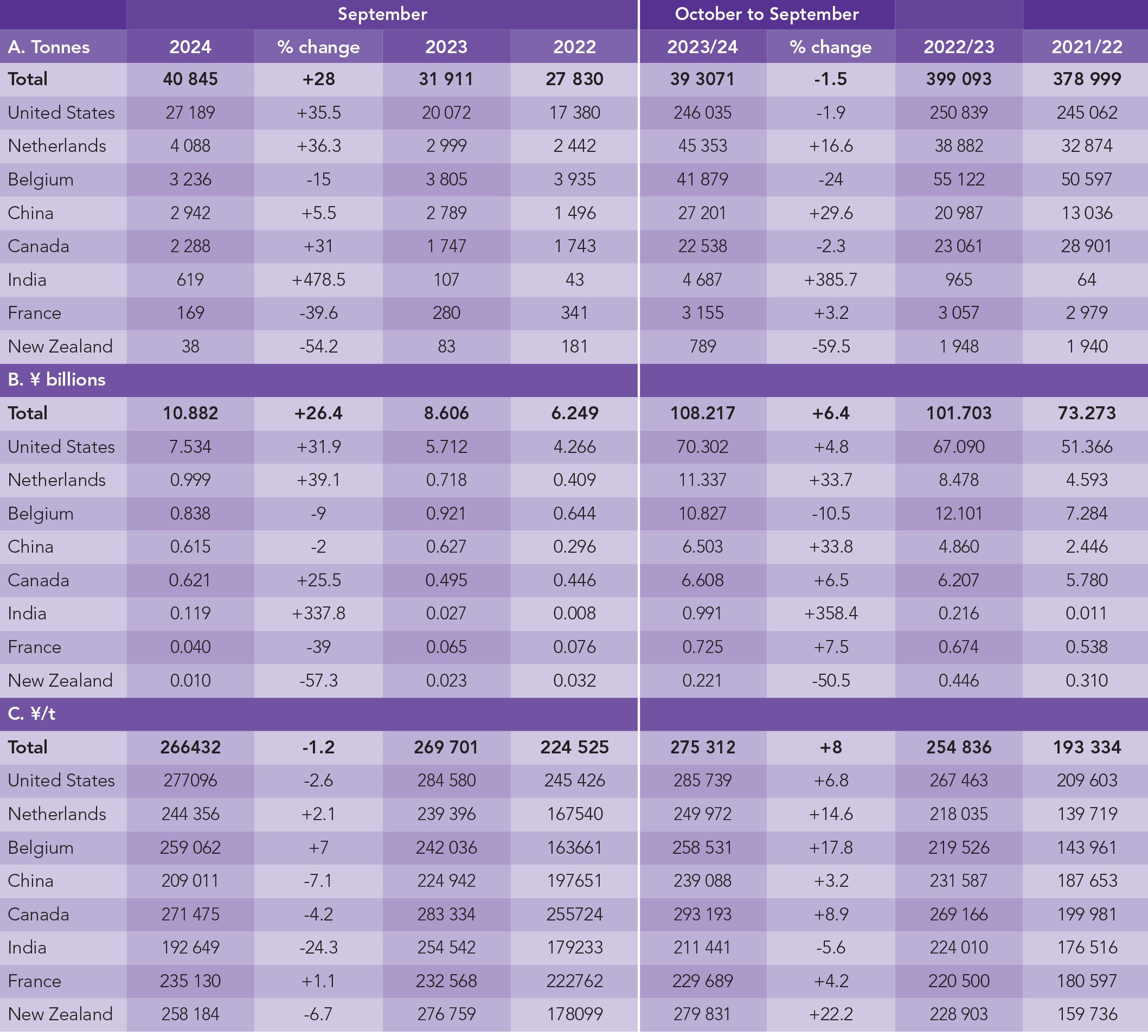

In September, Japan’s import price for fries fell below ¥270 000/t for the first time in a year, boosting demand. Imports surged to 40 845 tonnes, with the US expanding its market share at the expense of European suppliers. US fry sales increased by 35.5% from the previous year, while Canadian sales rose by 31%.

European suppliers, including Belgium and the Netherlands, reduced prices slightly but remained higher than the previous year. China and India offered highly competitive pricing, with Indian sales nearly five times higher than the previous year. Despite the increased imports, Japan’s fry market is still 1.5% smaller year-over-year but 6.4% higher in value, totalling ¥108.21 billion.

Table 1: Japanese imports of fries and other HS 200410 products (tonnes, ¥ billion, ¥/t). (Source: Trade Data Monitor LLC)

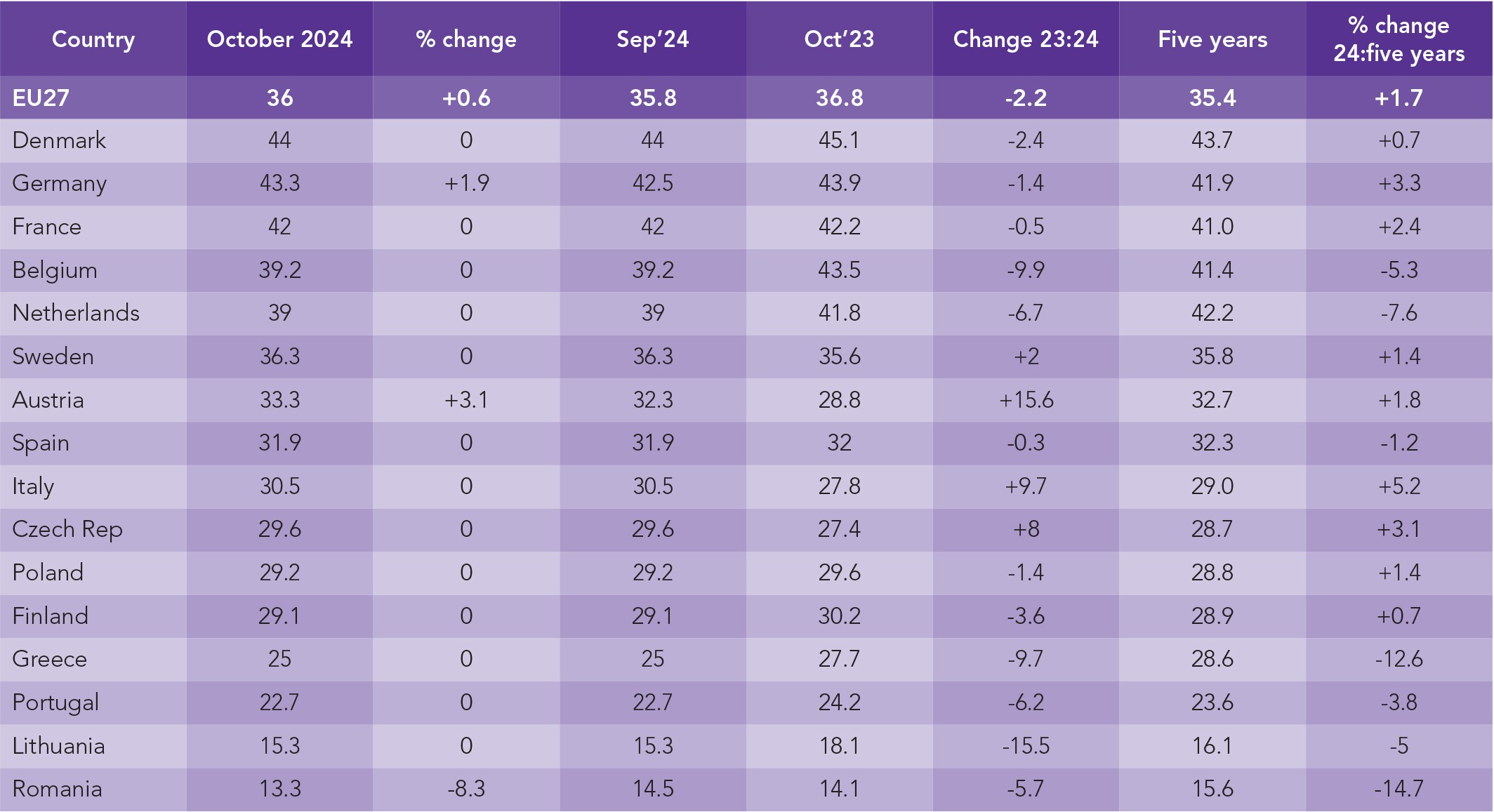

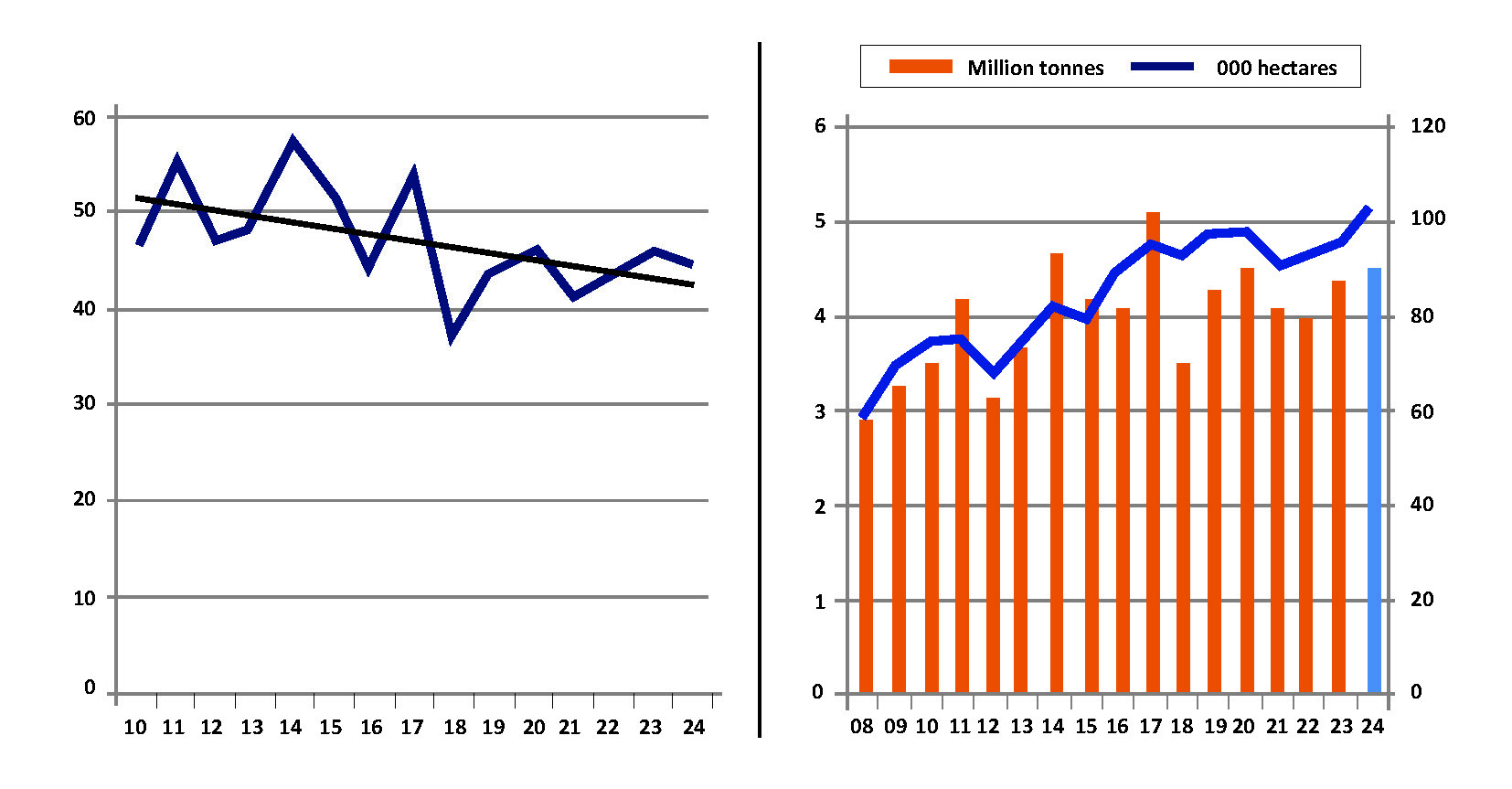

EU yields down

Despite a 2.2% decrease from 2023, EU potato yields remained 1.7% higher than the five-year average, according to the EU’s monitoring agricultural resources (MARS) service. Denmark led with 44 t/ha, though down 2.4%. Belgium and the Netherlands saw the largest declines, at 9.9 and 6.7% respectively, though Dutch national estimates showed a 3.5% yield increase.

French and German yields dropped by 0.5 and 1.4%. Italy had the highest yield increase (9.7%), while Lithuania saw the biggest drop (-15.5%). Poland’s yields also fell by 1.4%, differing from national estimates.

Figure 2: Dutch planted area of ware potatoes.

Netherlands: Rise in planted area

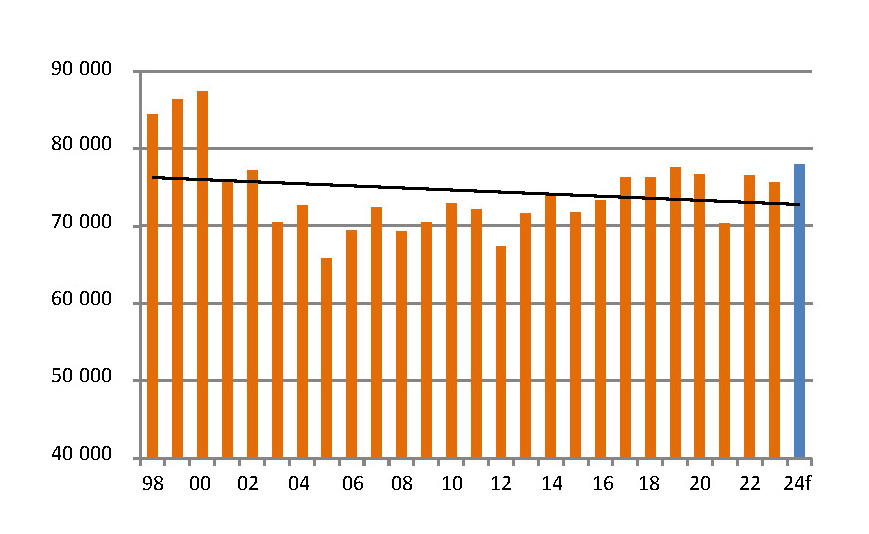

The Netherlands’ consumption of potatoes reached a four-year high in 2024, totalling 3.598 million tonnes, 6.5% higher than in 2023.

The planted area rose to 77 908 ha, the largest since 2019, with an average yield of 46.2 t/ha, up 3.5% from 2023. However, yields show a long-term decline, down from 50.8 t/ha in 2010 to 2014. Starch potato area decreased by 8.3% to a record low of 39 199 ha, while seed area slightly increased by 0.2%, the second smallest since 2014.

Table 2: MARS EU potato yield forecast 2024 in t/ha. (Source: EU MARS)

French potato market trends

Dry weather aided harvesting in France. Harvest supplies led to competitive prices, with processors favouring the Innovator variety, now priced at €180/t, a €50/t premium over other types. Processing prices were up €22/t from the previous year, though table potato prices have fallen, with Nord Basin Category I down €10/t to €470/t. Export demand, especially from Eastern Europe and the Netherlands, has driven up prices for bulk varieties such as Agata, rising €20/t to €320/t.

Figure 3: Average French weekly processing quotation (€/tonne).

German processing prices drop

Around 95% of Germany’s potato crop is harvested, with dry and cool weather expected to aid completion.

Processing prices fell slightly, with REKA averaging €152.50/t, down €10. Challenger and Fontane varieties averaged €120/t, while Innovator was at €185/t. Prices were below the previous year’s average when wet conditions caused a late harvest, and subsequent price rises in early 2024.

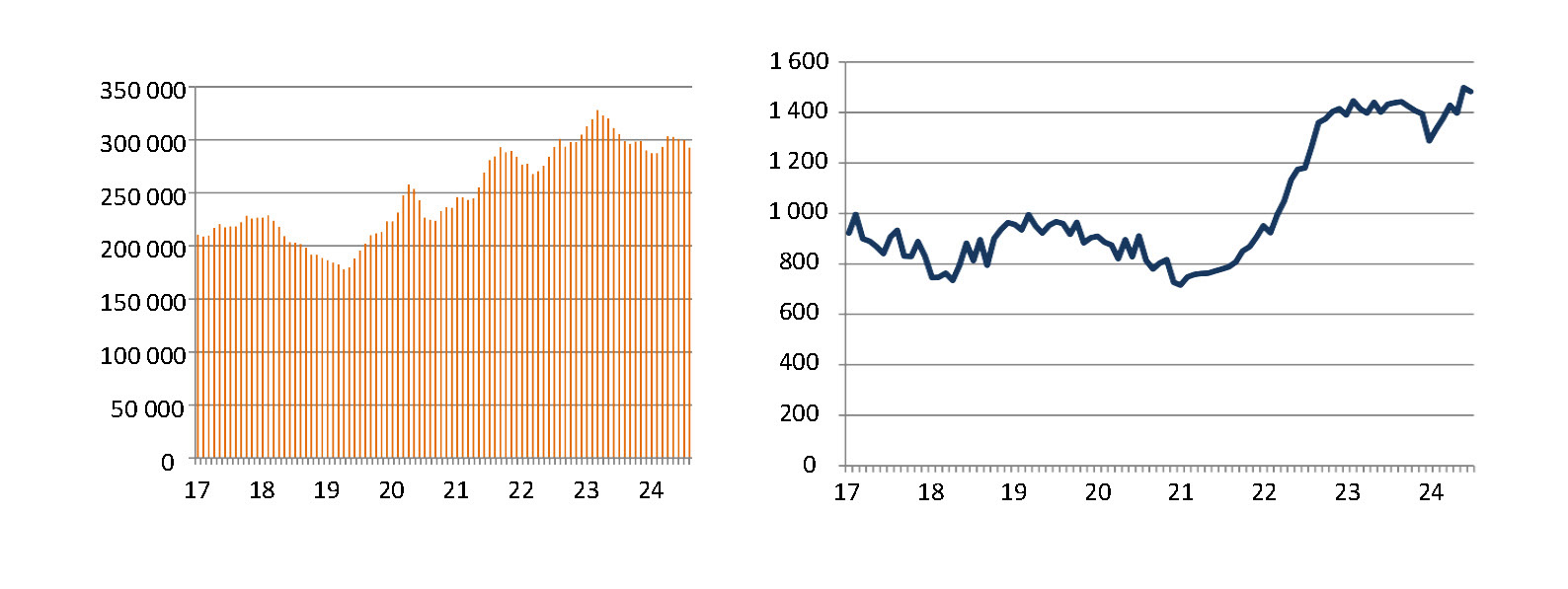

Production up in Belgium

Belgium’s consumption of potato production rose 2.5% to 4.550 million tonnes in 2024, though yields dropped by 3.1% to 44.7 t/ha.

The planted area increased by 5.8% to a record 101 805 ha. The country remains a major importer and exporter, with 3.768 million tonnes of fresh potatoes imported in the year ending July 2024. Key varieties such as Fontane, Challenger, and Innovator showed yield declines compared to 2023, while early varieties such as Amora and Sinora had higher yields. The market remains stable, with the Belgacom free-buy Fontane and Challenger prices steady at £125/t.

Figure 4: Belgian potato yield and Belgian areas and production of consumption potatoes. (Source: Fiwap/Carah/PCA)

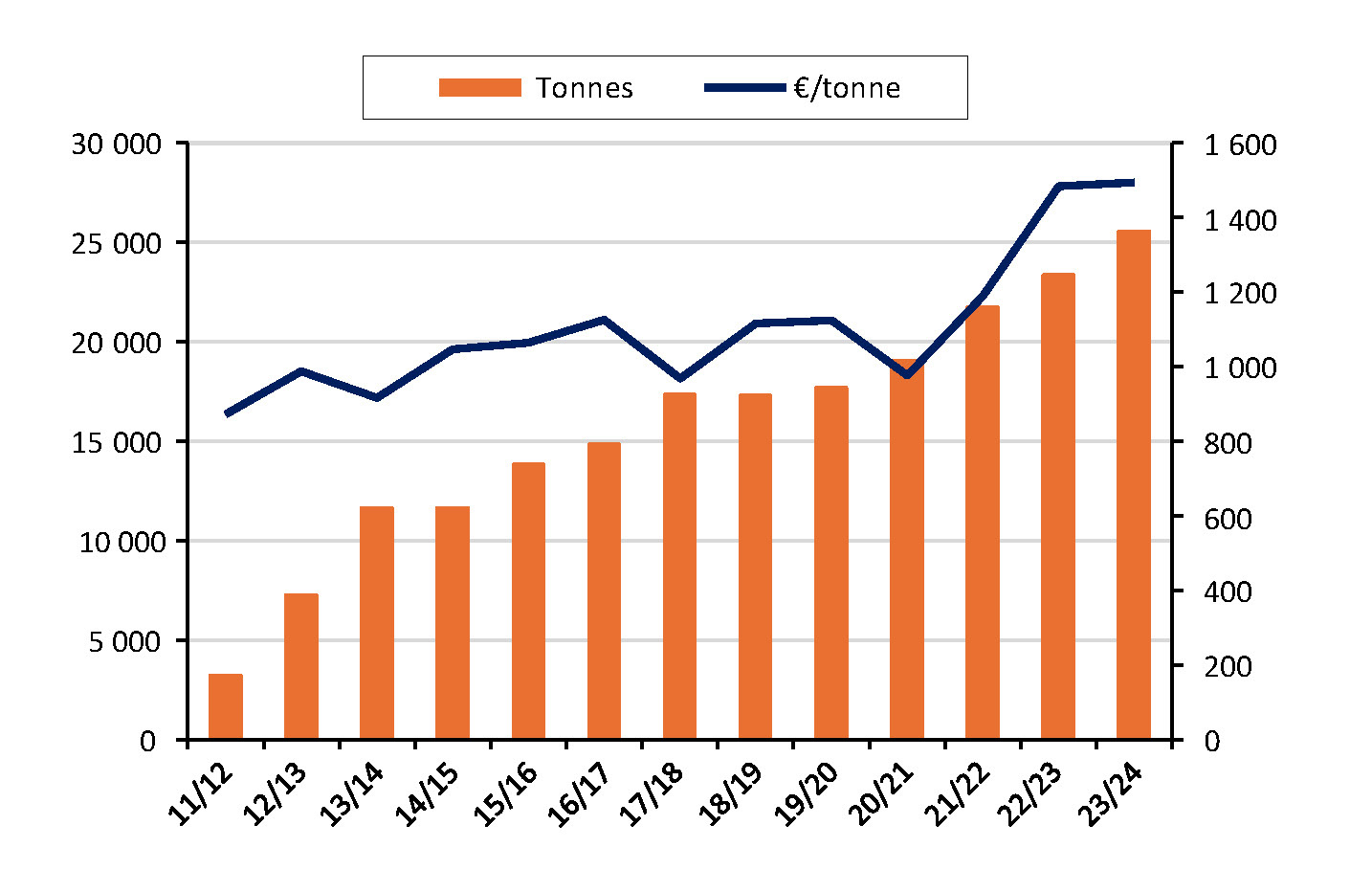

Polish potato prices rise

In the second half of October, Polish potato prices saw an upward trend, driven by higher export demand, especially for yellow and red varieties, which had previously seen greater price drops. The 2024/25 season is progressing with a lower supply as harvests near completion. While a significant portion of potatoes sold directly off the field were of poor quality and priced low, export demand is supporting price increases.

Although Poland’s potato exports are relatively small, with 52 000 tonnes exported in 2023/24, these sales have an impact on domestic pricing.

Yellow and red potatoes are currently priced between PLN 0.67 to 1.10/kg (€0.15 to €0.25), while white varieties range from PLN 0.93 to 1.50/kg (€0.21 to €0.35).

This marks a slight decrease compared to the previous but is expected to rise further, driven by better export demand and a poorer harvest. In smaller wholesale markets, potato prices averaged PLN 1.43/kg (€0.33), up from PLN 1.73/kg (€0.40) the previous year. Retail prices for 2 kg packs have risen by 24%, now averaging PLN 2.89/kg (€0.66), while bulk potato prices have dropped 27% to PLN 1.33/kg (€0.31).

Meanwhile, potato prices in neighbouring Ukraine and Moldova have been rising steadily, which could lead to early imports from Poland.

UK potato costs surge

The cost of growing potatoes in the UK rose by 1.4% in the year to September 2024. While production costs increased, retail prices saw a significant rise, up 19.25% over the past year due to lower volumes from the challenging 2023 harvest. Weather conditions and other external factors contributed to a difficult growing season.

The UK’s Agri-Inflation Index dropped by 2.6% from 2023, but it remains 120% higher than in 2006. Key input costs, including fuel electricity, crop protection products, and fertilisers, dropped by up to 21%, while costs for seed, labour, machinery, and contracts rose. Labour costs are expected to rise further due to a 4.8% increase in the national minimum wage.

Additionally, UK producers are facing significant financial challenges due to reductions in direct farm payments following Brexit. This has led to concerns regarding the impact on food production, with some producers being forced to sell land to cover tax liabilities linked to inheritance tax changes.

Despite these challenges, potato prices remain high due to short supply, with maincrop pre-packed potatoes priced between £270 and £400/t, depending on quality and variety. The average price for retail white potatoes in September 2024 was £0.92/kg, up 27.8% from the previous year, though still below the peak price of £1.03/kg in August 2013.

Saudi Arabia fry imports decline

In August 2024, Saudi Arabia’s frozen fry imports fell sharply to 14 252 tonnes, marking the lowest monthly total since August 2020 during the pandemic. This contributed to a 2% year-on-year decline in annual imports, totalling 293 012 tonnes. European suppliers are particularly concerned by this decline, as well as the rising competition from other countries. While Belgium remains the largest supplier, its shipments dropped by 67% in August, totalling just 1 726 tonnes. The Netherlands saw a 19.2% decrease in its August exports, down to 6 637 tonnes.

In contrast, Egypt and India saw substantial growth in their shipments to Saudi Arabia. Egypt’s exports surged by 71.4%, reaching 29 409 tonnes, while Indian exports grew by over 300%. These countries are offering more competitive prices, with Egyptian fries priced at €1 216/t and Indian fries at €1 357/t, compared to €1 396/t for Belgian fries and €1 625/t for Dutch fries. The establishment of fry processing facilities in Saudi Arabia is also reducing the demand for imports. Saudi Arabia has become an exporter itself, increasing shipments to neighbouring Gulf countries such as Kuwait, Bahrain, and the United Arab Emirates.

Figure 5: Saudi Arabia imports of frozen fries in 12-month periods (tonnes) and imports of frozen fries in €/tonne to Saudi Arabia.

Qatar’s fry imports

Qatar’s frozen fry imports increased by 9.3% in the year to August, reaching 25 541 tonnes. However, imports in August alone dropped by 21.8% compared to the previous year, with a significant decrease in orders from European suppliers. Dutch and Belgian exports to Qatar were down by more than 50% in August, although the Netherlands still maintained higher trade levels than Belgium. Egypt and India have been building a stronger presence in Qatar’s market, with Egypt recording 2 330 tonnes of fry imports and India showing notable growth from a low base in 2022/23.

Figure 6: Imports of fries in Qatar in tonnes and €/tonne

South Africa: Duties inhibit imports

South Africa’s imports of frozen fries saw a significant decline over the past year due to increased duties on European imports, but September 2024 marked an uptick. September’s import total of 3 020 tonnes was the highest since July 2023, with

Belgium being the dominant supplier, providing 3 012 tonnes. However, this was still a 74.9% drop in imports for the year to September, with Belgium’s shipments declining by 75.9%. Other countries such as India, Zambia, and the Netherlands also experienced a reduction in demand, while the US saw a small increase in exports to South Africa, totalling 326 tonnes.

Despite a 1.9% overall price increase in imported fries over the past year, the price for September was lower, at R22 214/t – 16.8% less than the previous year. The reduced imports have not resulted in an increase in South African fry exports, which dropped by 17.2% for the year, totalling 7 481 tonnes, and fell 51.3% in September to just 498 tonnes.

Namibia and Botswana were the top destinations for South African fry exports.

Regarding ware potatoes, South Africa exported 135 468 tonnes in the past year, a 7.3% decrease compared to the previous year. Mozambique was the largest destination, accounting for 60% of these exports, followed by Namibia (15%) and Eswatini (9%).

Figure 7: South Africa fry imports in tonnes.

Figure 8: Unit value of South African fry imports in rand/tonne.

India leads Thai fry market

India has strengthened its position as the dominant supplier of frozen fries to Thailand, accounting for 61% of the total fry imports in September 2024.

This represents a significant 57.9% increase in fry shipments compared to the same month in 2023. India’s sales for the year have risen by 28.3%, and they now control 47% of the total fry import market. Despite price increases, with India raising its price by 9.4%, it still outpaced competitors, earning a significant revenue of Bht 194.814 million (US$5.73m; €5.29m).

China’s sales have seen a drop of 21.8% in the annual total despite reducing its fry prices by 14.4%, making Chinese fries cheaper than the previous year. However, their September sales were lower by 325 tonnes, and they are now the second-largest supplier after India.

New Zealand saw a good month in August but faced a significant drop in September due to a Bht 2 800 price hike. Despite this, their annual sales have increased by 20.1%.

The Netherlands, which cut its price by Bht 2 400, also saw no growth, with sales falling by 508 tonnes in September.

Overall, the total value of the Thai fry import market dropped by 7.5% compared to the previous year, totalling Bht 4.037 billion (US$119 million; €110 million). Additionally, there has been a significant increase in fresh potato imports to Thailand, especially from China. Chinese fresh potato imports grew by 54.6%, amounting to 43 779 tonnes over the year, making them the leading supplier in the market.

Figure 9: Average price of Thai fry imports in baht/tonne.

Belgium boosts Chilean fry sales

In September 2024, Belgium maintained a strong presence in the Chilean fry market, boosting its sales significantly. Belgian imports increased by 17.4% year-on-year, reaching 4 859 tonnes. This surge was aided by a price reduction, with Belgian fries priced at US$1 357/t (€1 247/t), which was 7.4% cheaper than the same period in 2023. Overall, Chile’s total fry imports for the month reached 846 tonnes, an 8.2% increase compared to the previous year.

Despite price cuts from Argentina, where the cost fell by US$155 to US$1 768/t (€1 625/t), Belgian fries were more competitively priced, leading to higher sales. Argentina’s fry sales increased by 42.8% in September, reaching 1 745 tonnes, but their 12-month sales were still down by 26.6% compared to the previous year.

The Netherlands also saw an uptick in sales, with a 19.9% increase in September (1 367 tonnes), despite raising its price to US$1 548/t (€1 423/t). However, its total sales for the year remain 10% below levels seen in 2021/22.

Brazil and China are emerging as important price competitors in the Chilean market. Brazil, at US$1 415/t (€1 300/t), offers a much cheaper alternative than Argentina, with a 42.8% price gap. Brazil’s 12-month sales reached 1 304 tonnes. China, with the lowest price at US$1 251/t (€1 150/t), shipped 68 tonnes in September, bringing its annual sales to 460 tonnes.

Germany, the fourth largest supplier, also showed positive growth with an 18% increase in 12-month sales (7 991 tonnes), though its price of US$1 410/t (€1 296/t) is competitive.

Overall, Belgium’s competitive pricing and consistent supply helped maintain its strong foothold in Chile’s fry import market, despite the rising presence of lower-cost suppliers such as Brazil and China. – Francois Strauss and Jodie Hattingh, Potatoes SA

For more information, email the authors at francois@potatoes.co.za or jodie@potatoes.co.za.