Estimated reading time: 15 minutes

In August 2023, North American potato supplies were increasing, and the United States (US) experienced the second-largest monthly volume of fry exports. Despite an almost 3% dip in retail sales volume, the value surged by 17%.

Canada was set for a record harvest, easing potential supply issues. Germany’s potato market remains robust, and Spain saw increased production despite planting the smallest area. In the US, fry and frozen product exports showed signs of recovery for the 2023/24 season. While Asian Pacific markets faced pressure, South Africa and Australia continued to demand more fries.

US fry prices surged by nearly 30% last year, reaching a 12-month average of US$1 586/tonne. Despite a decline in demand from key Asian Pacific markets, exports to China doubled.

Mexico witnessed increased demand, with ware exports rising by 10.6%.

The US imported 103 870 tonnes of fries in August, while its retail volume sales dipped but values soared, reaching a new record of US$16.941 billion in the year ending June 2023.

Lamb Weston experienced a 47.9% increase in sales, reaching US$1.665 billion in the July to September period. North American sales rose by 19%, with a 24% price increase and a 5% drop in volume. International sales surged by 212%, with prices up 18% and volumes up 194%. Lamb Weston raised its earnings target for the year, anticipating sustained demand and a favourable pricing environment. The company remains optimistic about the potato crop in North America and Europe, emphasising strategic investments for long-term growth.

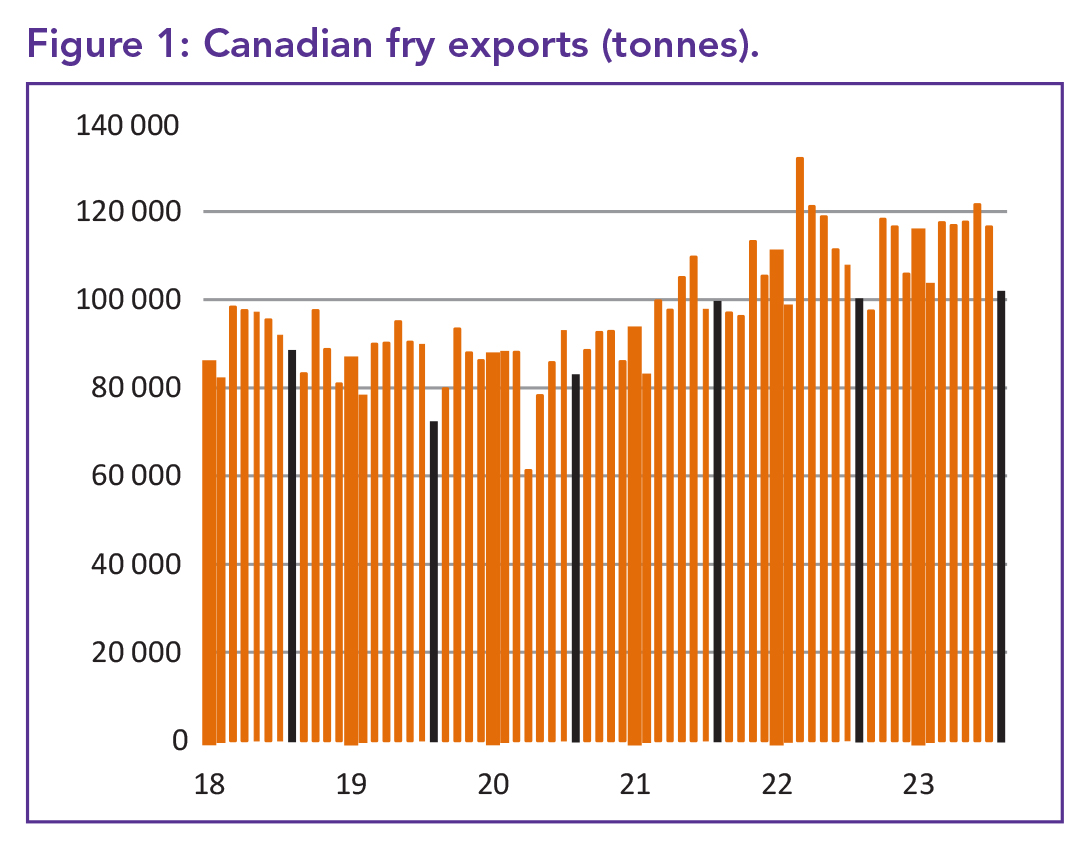

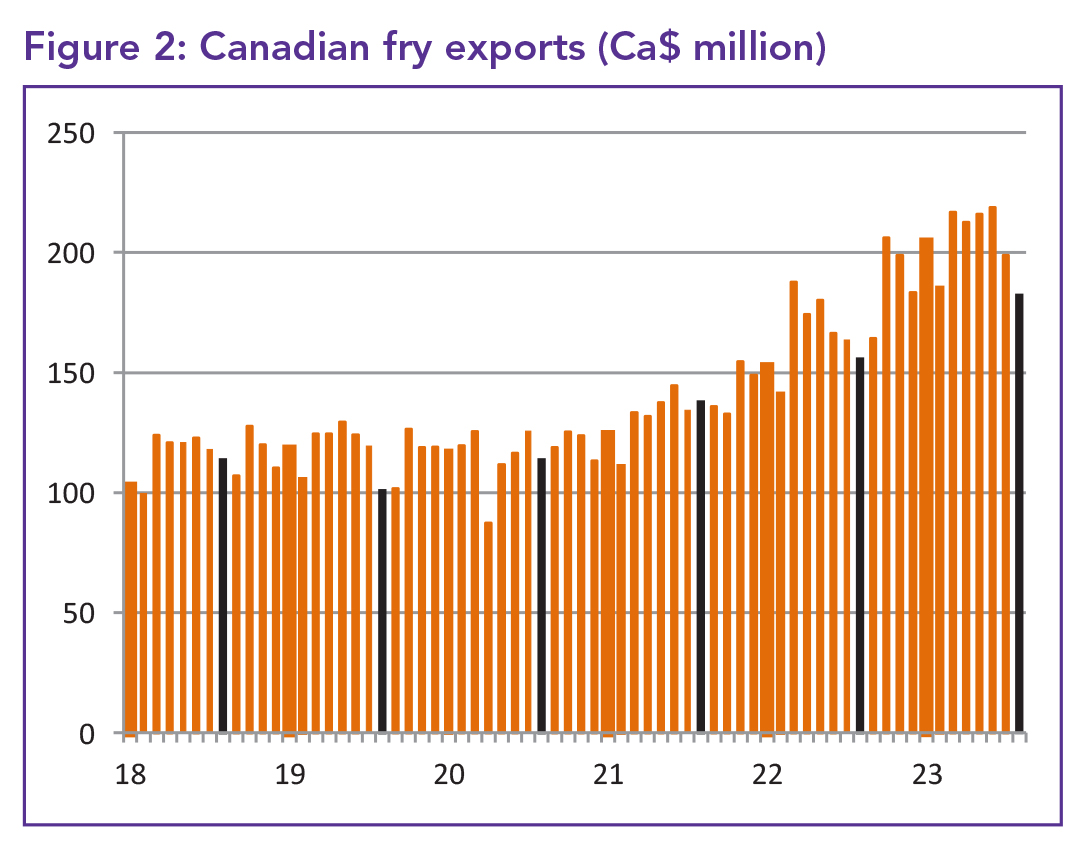

Canada: Export records reached

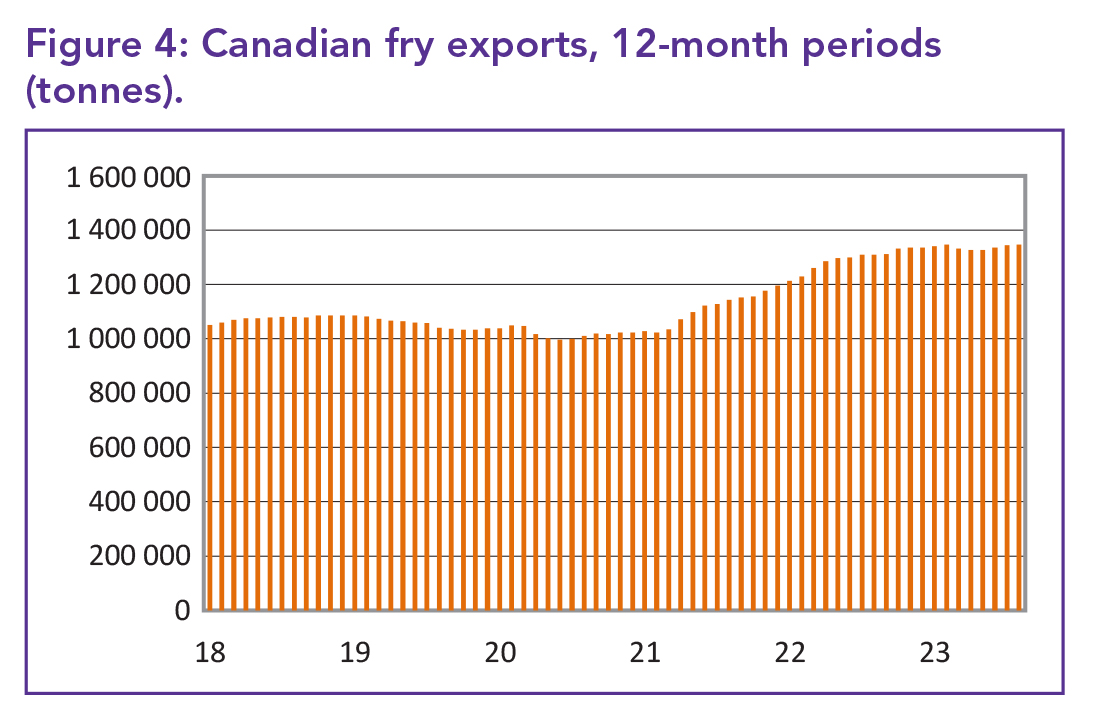

North American exports have enabled Canada to sustain record levels of frozen fry exports. In August last year, 101 663 tonnes were shipped, a 1.7% increase from August 2022, with 12-month exports up 2.8% to 1.348 million tonnes. The US accounted for 87.6% of these exports and 88.1% over the year, experiencing a 3% demand increase to 1.187 million tonnes.

Market performance varied, with a 2.1% annual sales increase to Mexico and a significant 19.1% decline in Japanese demand over the year. South Korean sales, however, rose by 22.4%, and the United Kingdom (UK) witnessed a substantial 606% increase in exports to 9 546 tonnes over 12 months.

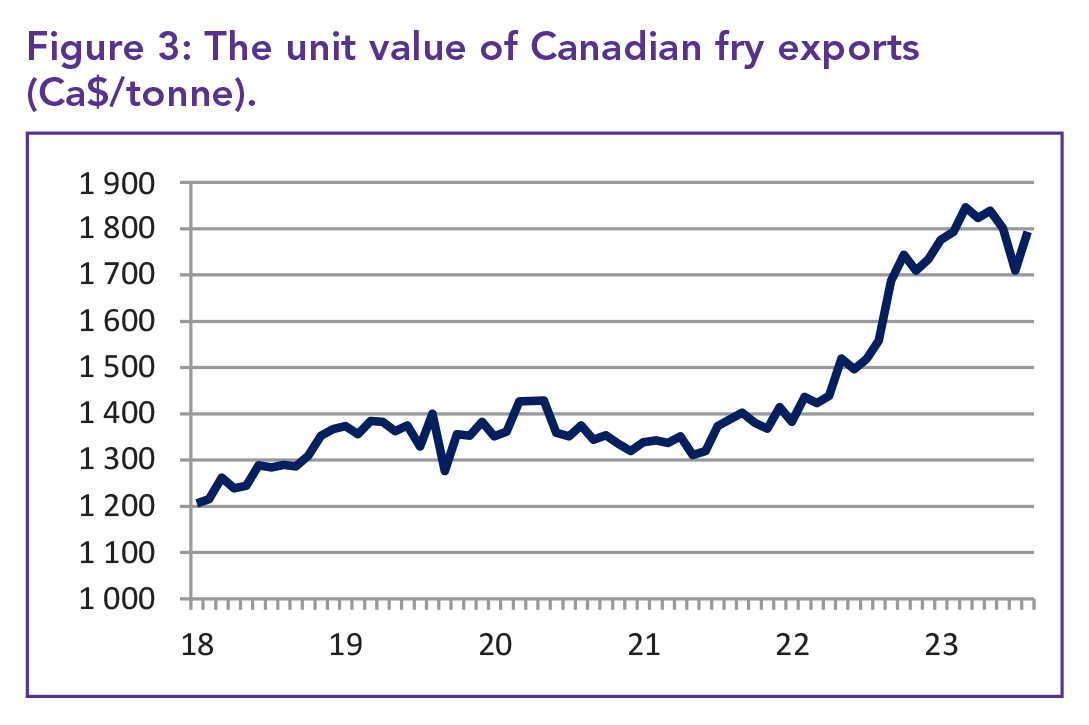

The US remains the highest-priced market for Canadian fries, with average prices reaching Ca$1 852/tonne (€1 287 or US$944) in August.

This compares to Ca$1 793/tonne (€1 246 or US$914) for the overall average and Ca$1 269/tonne (€882 or US$93) for exports to Taiwan.

Despite challenges such as drought and heavy rain, Canada expected a record national crop of 5.760 million tonnes, a 3.3% increase from 2022. Alberta led with a 17.3% increase to 1.426 million tonnes. Manitoba followed with an 8.1% rise to 1.282 million tonnes, and Saskatchewan saw a 20.6% increase. Prince Edward Island faced wet conditions, resulting in a 1.1% production drop. The eastern Maritime region experienced a 2.8% decrease to 1.936 million tonnes, while Quebec expected a 13.9% drop in production to 579.646 tonnes due to heavy rain.

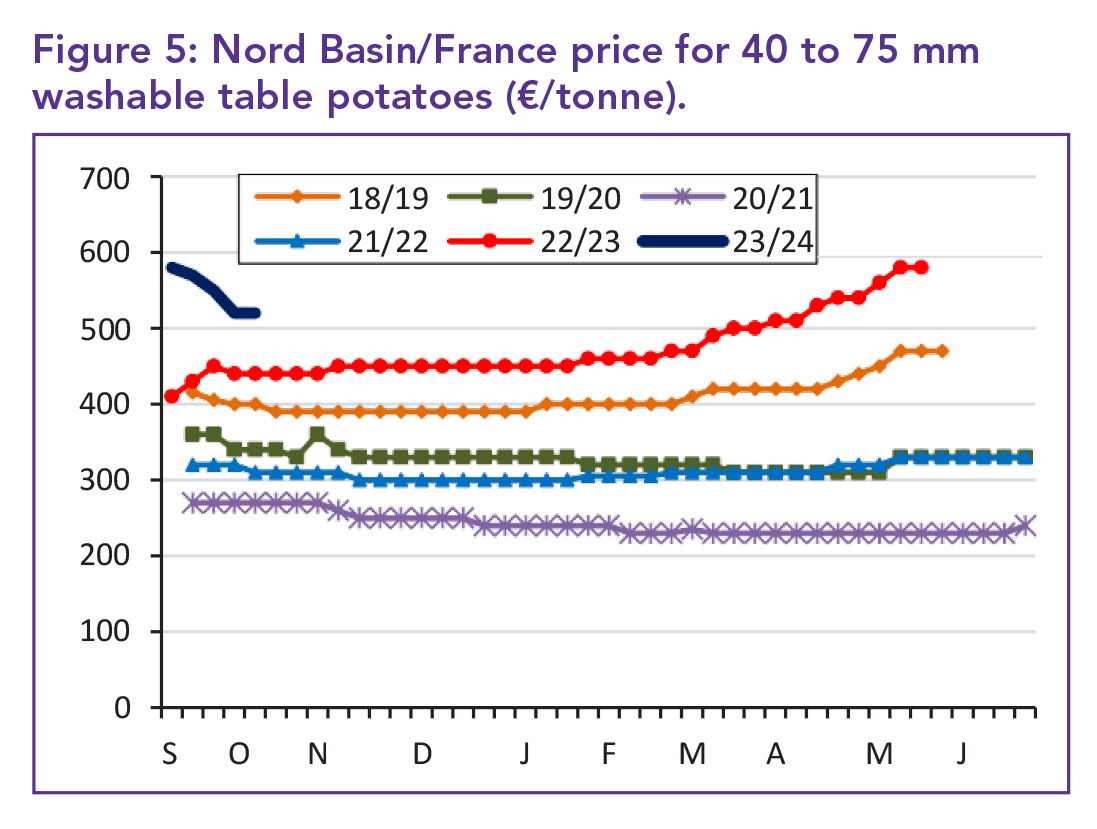

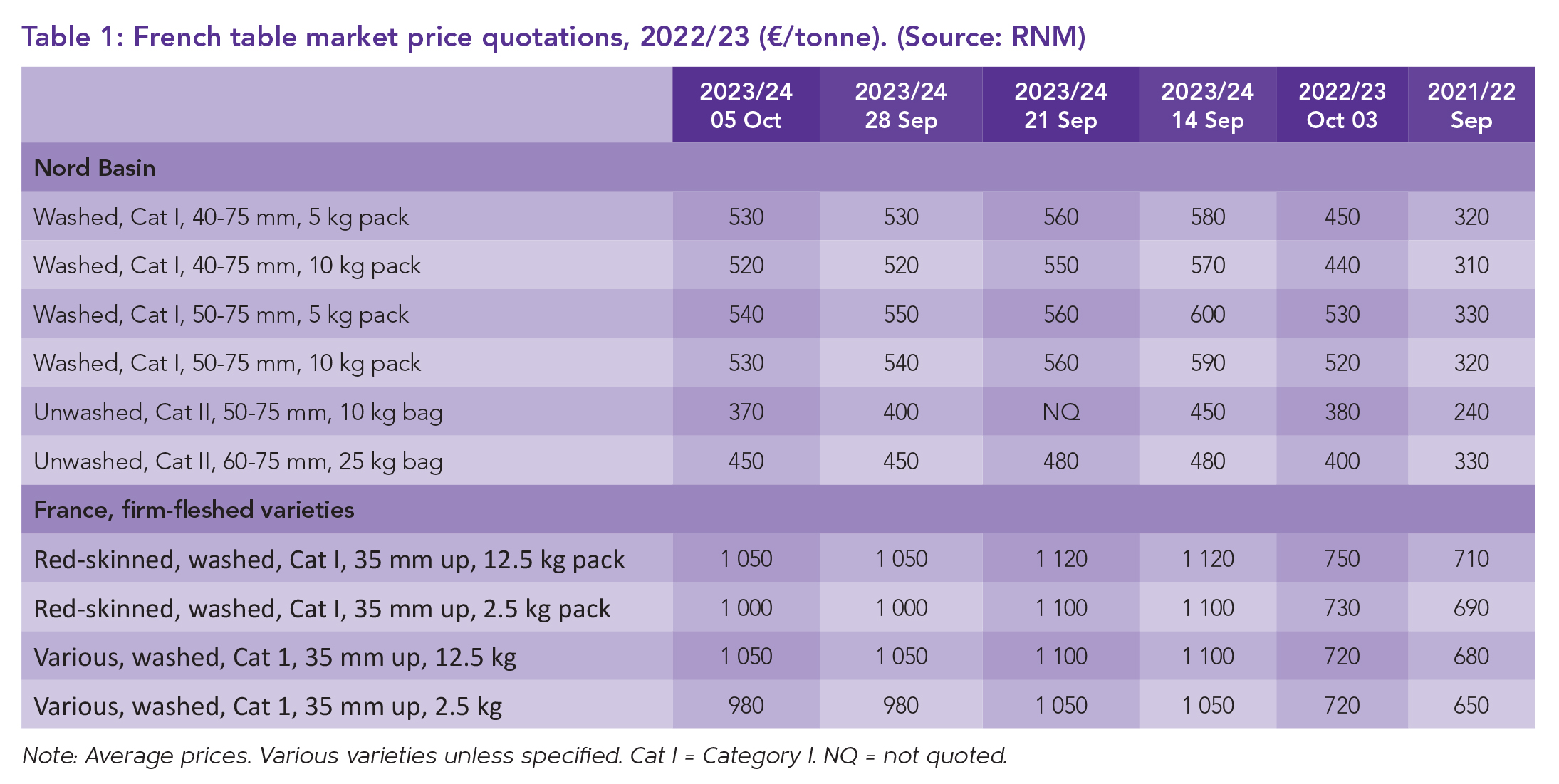

France: Rain aids harvesting

Hot weather has slowed the demand for table potatoes in France. Despite initial high season starting prices, table potato prices stabilised. The elevated temperatures deterred shoppers from purchasing potatoes, while growers took advantage of the dry weather to harvest. Maintaining the coolness of lifted potatoes posed a challenge, making the temperature drop a welcome relief.

The northeast of France anticipated some showers which could aid harvesting conditions, although a return to sunny and dry weather was also forecast, accompanied by a decrease in temperatures to highs of 15°C.

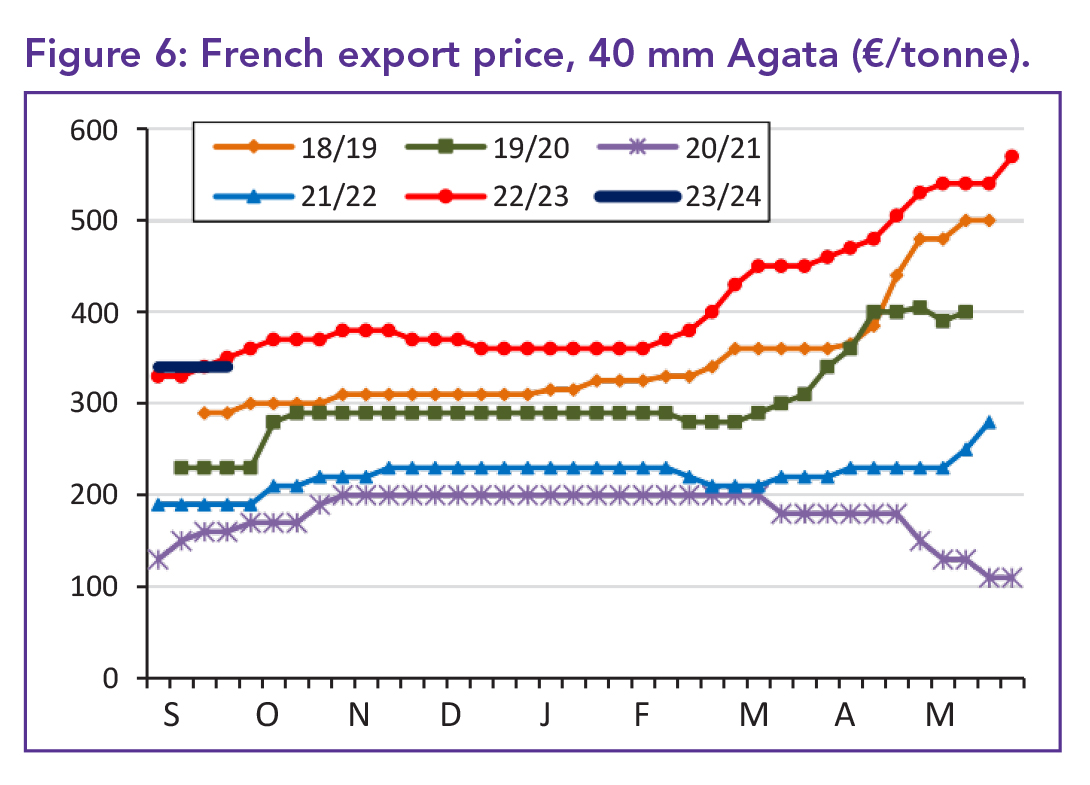

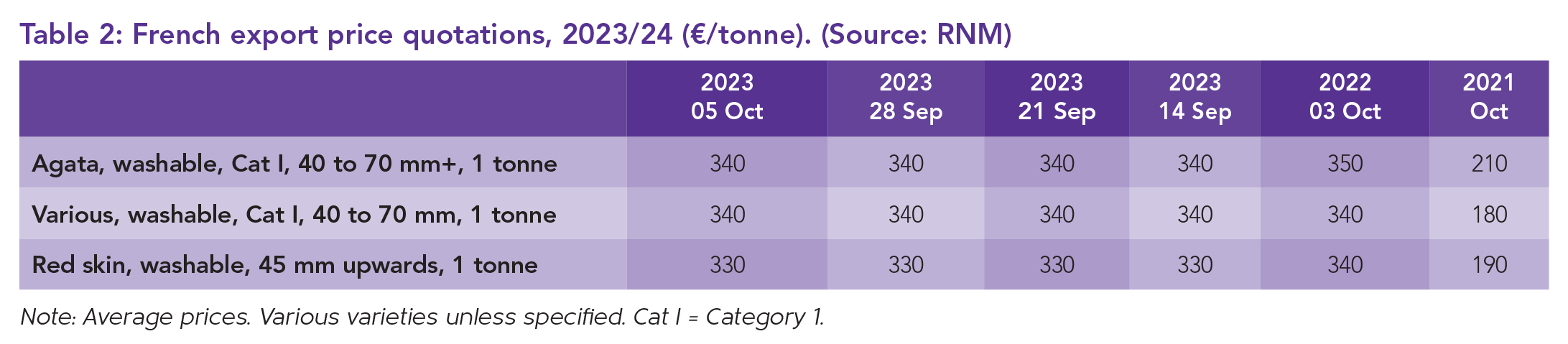

Export potato prices for bulk loads of Agta held at €340/tonne, slightly below the levels from the previous year. There was ongoing interest in French potatoes in the country’s main export markets, with exporters actively selling at events like the Fruit Attraction show in Madrid. Spain stood out as the most crucial export market for French table potatoes.

Processing potato prices remained steady, standing at €100/tonne for Fontane and other primary processing types, with a €10/tonne premium for Innovator, as reported by pricing agency, RNM.

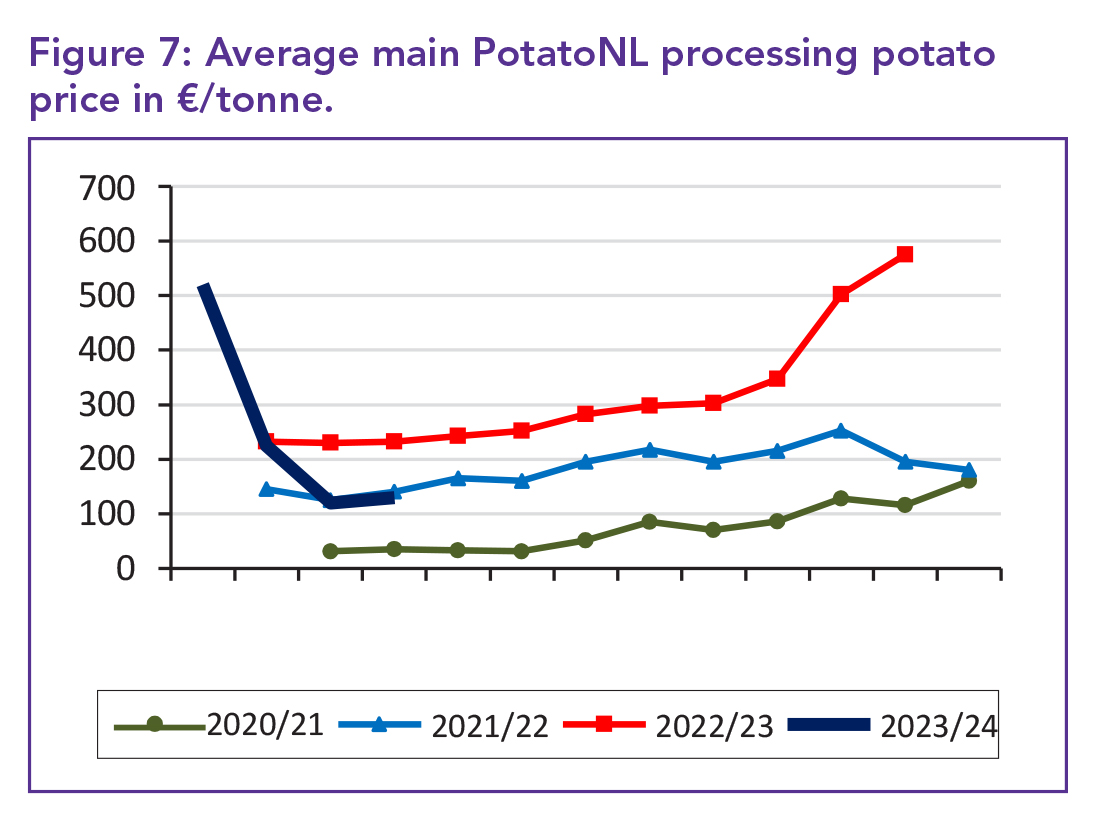

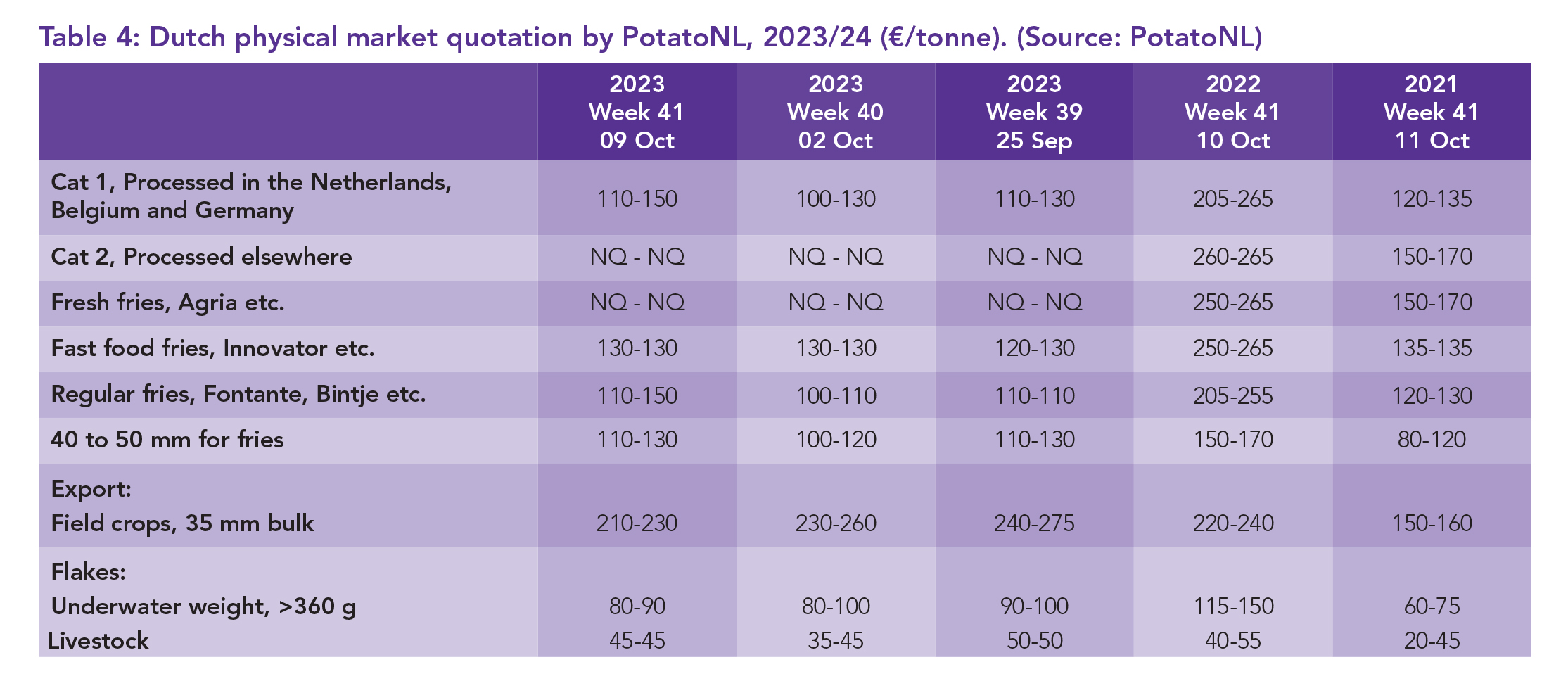

Netherlands: Prices stabilise

After weeks of declining prices, there was a sense of optimism as values stabilised and even exhibited signs of increase. The main PotatoNL price quote averaged €230/tonne within a range of €110 to €150/tonne. This reflected a €15/tonne increase from the previous week when the range was €100 to €130/tonne. Prices in other major categories also rose by as much as €25/tonne, indicating heightened competition for free-buy stocks among processors.

While prices were approximately €100/tonne lower than the previous year, they did align with the 2021/22 season when values started to rise post-Christmas.

Trial digs suggested yields slightly below the five-year average, but there was a higher-than-average proportion of 50 mm+ potatoes. Dry matters were below the five-year average, impacted by quality issues, including elevated levels of blight.

This left vulnerable potatoes seeking quick market placement, while growers were storing higher-quality material to fulfil later-season contracts or capitalise on anticipated increases in free-buy prices.

Harvesting conditions remained favourable, though cooling hot potatoes to storage temperatures presented challenges.

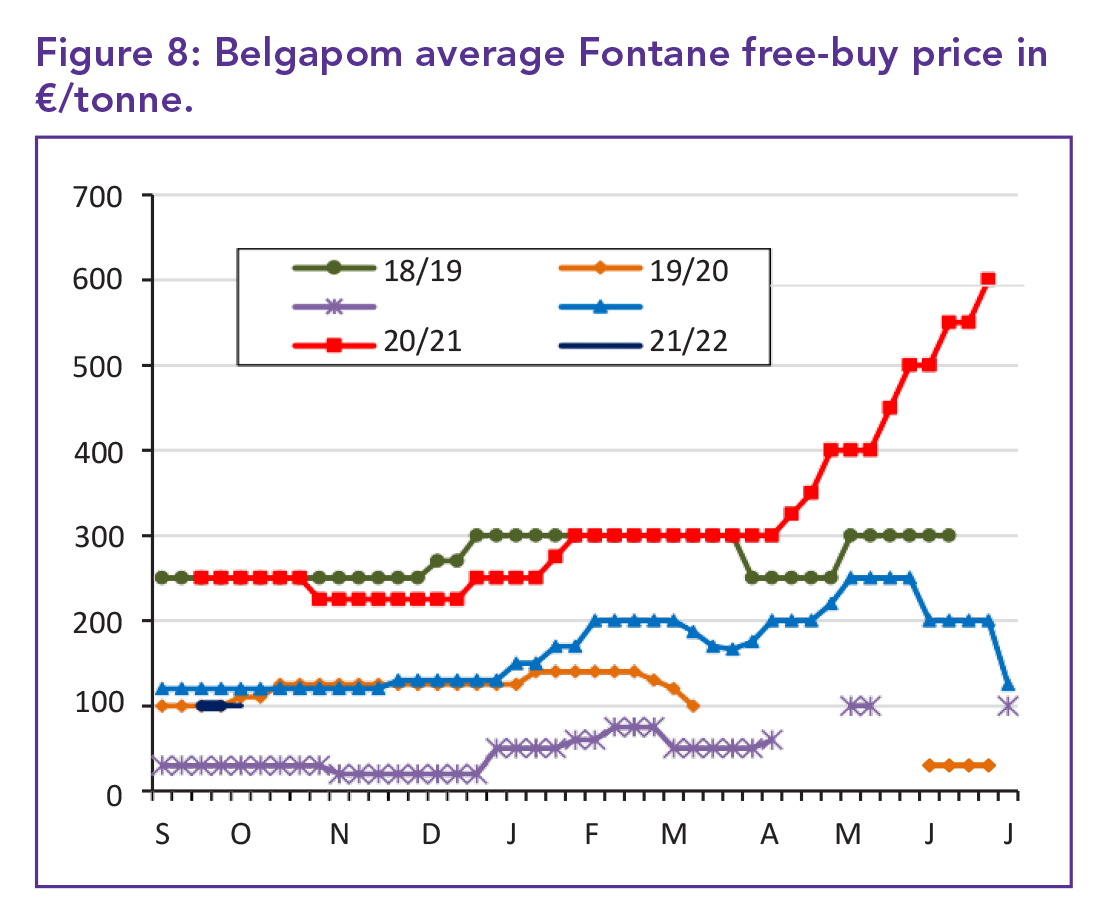

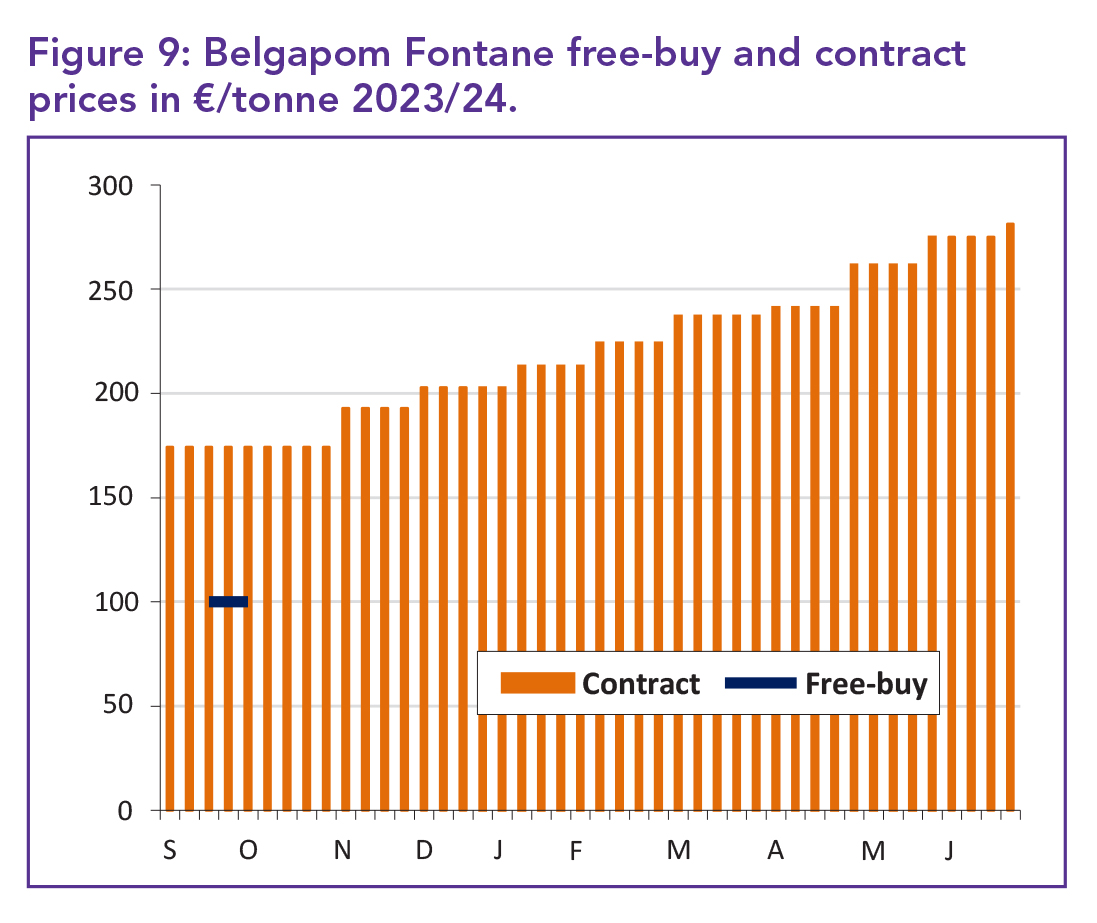

Belgium: Quality concerns

Belgium continued to grapple with a surplus of free-buy potatoes, exerting downward pressure on prices.

Better-than-expected yields helped to meet contract requirements but concerns regarding quality prompted growers to swiftly move their at-risk stocks. Export potato demand provided some support to the market. Despite the surplus, there was an anticipation that prices would rise once harvest supplies were depleted, and growers wanted to fulfil their contract commitments.

The Belgapom free-buy price for Fontane and Challenger remained at €100/tonne, with supply meeting demand. However, the PCA/Fiwap price was slightly more bearish, averaging €90/tonne for Fontane and Challenger within a range of €80 to €100/tonne. Bintje, used for fresh fries in Belgian consumption, commanded a premium with an average price of €112.50/tonne in a range of €100 to €125. Innovator and Agria had no quoted prices.

Prices were lower than those in the 2022/23 and 2021/22 seasons, though similar to values at the same point in the 2019/20 season. The average free-buy Fontane price remained approximately €75/tonne below the average contract price. If this trend persisted during growers’ planting decisions for 2024, it may have influenced planting choices in spring.

Germany: Strong demand continues

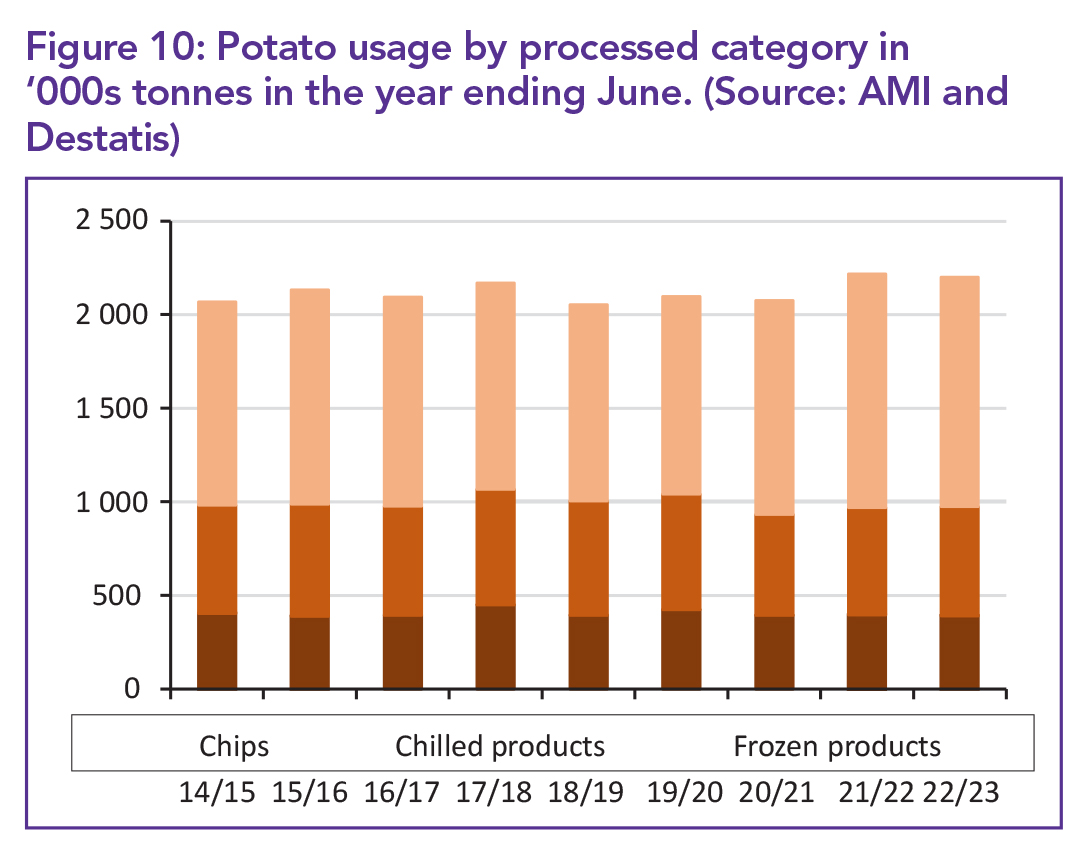

Germany continued to experience strong demand for processed potato products, with usage just below the record of the previous season in 2022/23, according to figures from the national statistics office, Destatis. In the 12 months to June 2023, 2.2 million tonnes of potatoes were used for processing, a 0.8% decrease from 2021/22.

Usage for frozen fries and other products was at 1.225 million tonnes, down by 1.8% from 2021/22.

Chips/crisps usage decreased by 1% to 393 000 tonnes, while usage for chilled products increased by 1.7% to 582 000 tonnes. Last year saw no usage for dehydrated products, which was the largest category in the 2021/22 season at 1.592 million tonnes.

Production of frozen, chilled, chip/crisps, and potato salad products reached 1.121 million tonnes, a record for the group of four and a 4.9% increase from the previous year. Potato salad production more than doubled to 69 000 tonnes, with an 8.7% increase in chilled products to 324 000 tonnes. Chip/crisp output decreased by 0.9% to 116,000 tonnes, while frozen fries and other products decreased by 1.9% to 612 000 tonnes.

Prices for frozen fries rose by 40%, chip/crisp prices increased by 25%, chilled products prices rose by 21%, and potato salad prices saw a 20% increase.

Processing potato prices remained steady, with the lowest price quote by the Rhineland organisation at €100/tonne. Harvesting progressed well with good conditions reported across the country. Some table potato lifting was completed. The forecast was for some showers, which should not significantly delay harvesting and may have helped soils that were drying out. However, the favourable weather for harvesting was not conducive to promoting table potato consumption.

Spain: Price decrease anticipated

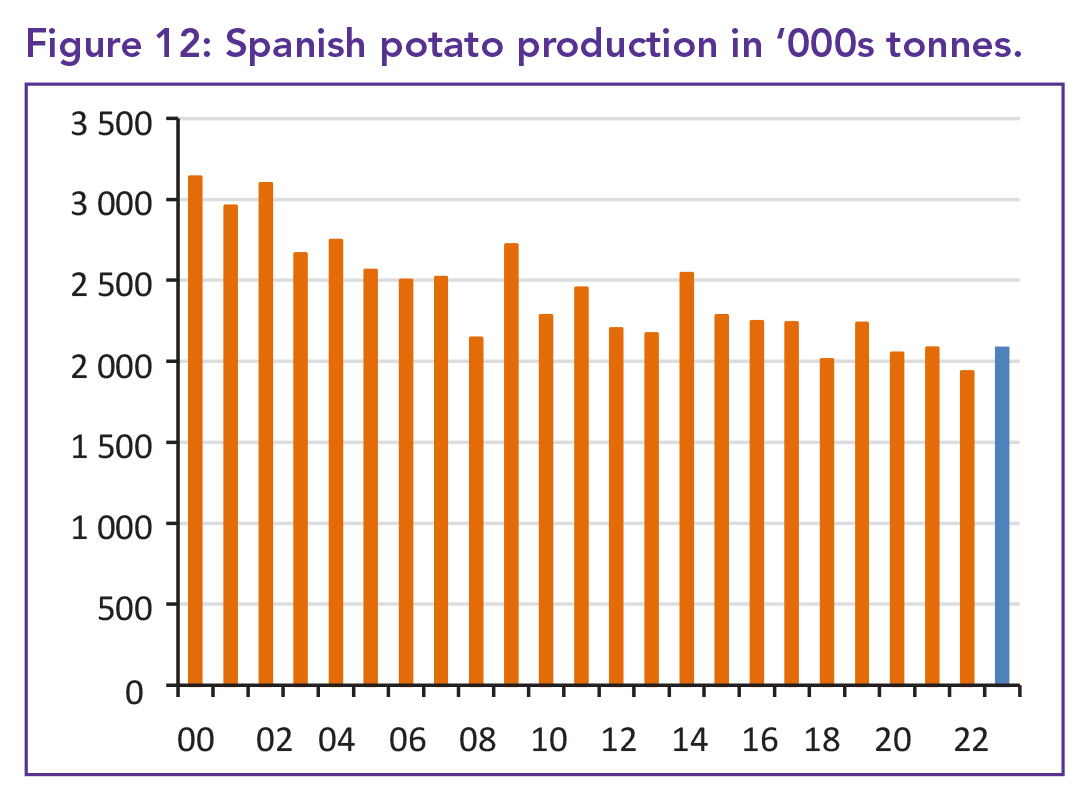

Spain witnessed a bigger middle-season potato harvest in 2022, reaching 835 437 tonnes from 28 708 ha, a 2.4% increase compared to the previous year. The average yield for the middle season crop was 29.1t/ha, marking a 6.6% increase from the previous year. The early potato harvest, however, was revised downward to 397 767 tonnes from 12 914 ha, with an average yield of 30.8t/ha, a 3.5% decrease from the previous year.

Late-season potatoes in Spain were also revised downward to 17 278 ha but still recorded a 1.1% increase compared to the previous year. Castilla y Léon, the main producing region, reported 11 419 ha of late potatoes, a 3.1% increase from the previous year.

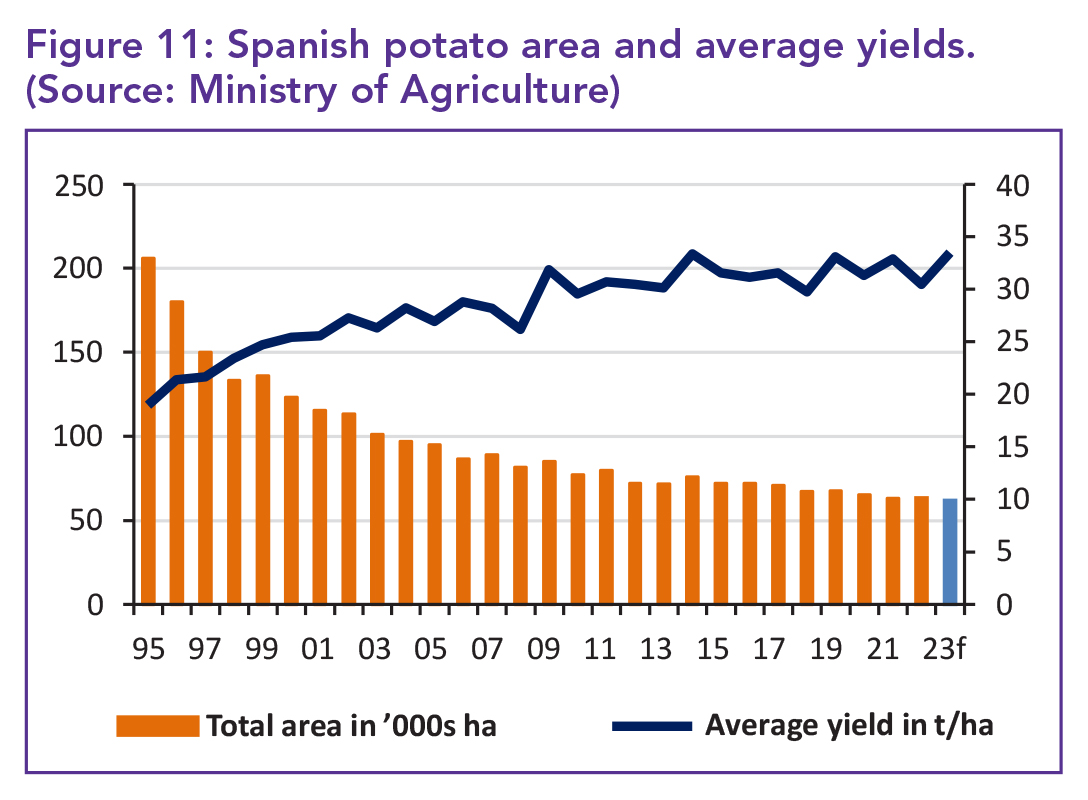

Despite the revisions, the total Spanish potato area was at 62 052 ha, 2.3% below the previous year and the smallest on record.

The ex-farm potato price in Spain decreased by 1% to €365.20/t in the week ending 1 October, the second-highest price for that time of the year since 2018. Prices at Lonja de León decreased, with all varieties sold at €300/t except for Agria at €330/t on 4 October. This price decline was attributed to French potatoes entering the Spanish market.

Emiliano Marcos, the commercial manager at Interagro de Patatas in Castilla y León, anticipated further decreases in potato prices in the free-buy market due to the pressure from France to sell potatoes with poor quality across Europe.

Portugal: Potted plants promoted

In Portugal, the average ex-farm price of white-skinned ware potatoes stood at €300/t in the week ending 1 October, remaining consistent with the previous week. However, it reflected a 20% decrease compared to the same week the previous year and a 17.6% increase compared to the average price in the triennium from 2019 to 2021, according to SIMA-GPP.

Specifically, the ex-farm price of ware potatoes was €300/t at Guarda, Beira Litoral, and Entre Douro e Minho markets, while it was €400/t at Viseu market in the week ending 8 October.

Meanwhile, Elsner Pac, a German breeder and producer of ornamental plants, introduced a new method of planting potatoes in Portugal. The company’s Portuguese subsidiary in the Peninsula de Setúbal region is producing potted potato plants, including gourmet varieties with blue and purple skin and flesh. These potted plants can fetch up to £5.45 a pot in the UK.

Sérgio Figueiredo, manager at Elsner Pac Portugal, notes that while rooted plants were 5% less productive, they feature more uniformed tillers, grow more quickly and have a production cycle four to five weeks shorter than seed potatoes. This approach leads to savings in water, energy and pesticides.

Elsner Pac Portugal aims to conduct field trials in Portugal and Spain to compare the performance of potatoes produced with rooted plants versus seed, and the company is seeking producers to host these trials. In addition to potato plants, Elsner Pac Portugal also produces 45 million cuttings of ornamental, aromatic, and potato plants.

UK: Bagged potatoes in demand

Divergent weather conditions have significantly impacted the potato industry. Southern regions experienced dry and very warm conditions, with temperatures exceeding 25°C, while Scotland faced heavy rainfall, reaching more than 170 mm in some areas.

Some eastern growers in the UK had to irrigate before harvesting due to dry soils, but favourable conditions in England allowed for steady progress. Yields were reported to be around average and better than anticipated given the late planting season.

Growers were primarily focused on storing potatoes rather than selling them, helping to maintain prices. Maincrop prices ranged from £200 to £370/tonne, as per Potato Call’s European and UK Review. Prices were expected to increase further throughout the season, particularly if there were supply issues from Scotland.

The warm and sunny weather in England positively impacted fish and chip sales at the end of October, reinforcing demand for bagged potatoes, which were fetching up to £300/t depending on location and variety. Scotland anticipated experiencing a welcome period of drier weather.

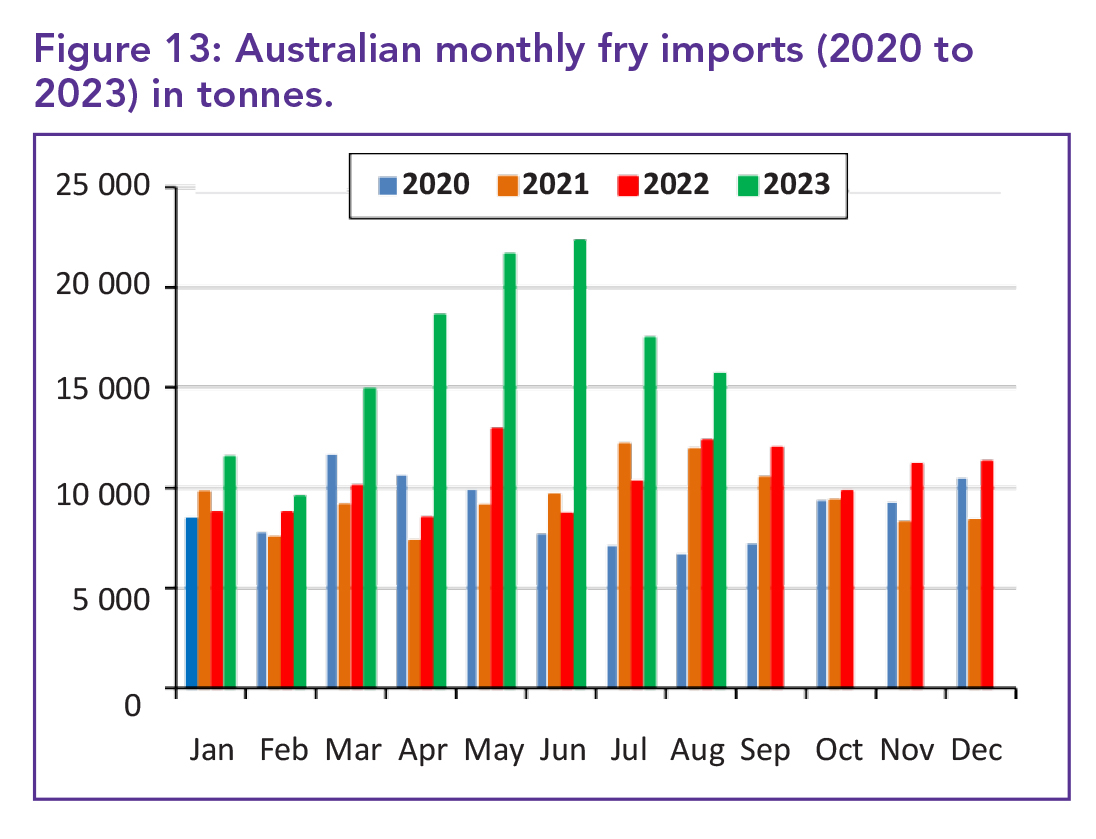

Australia: High fry prices

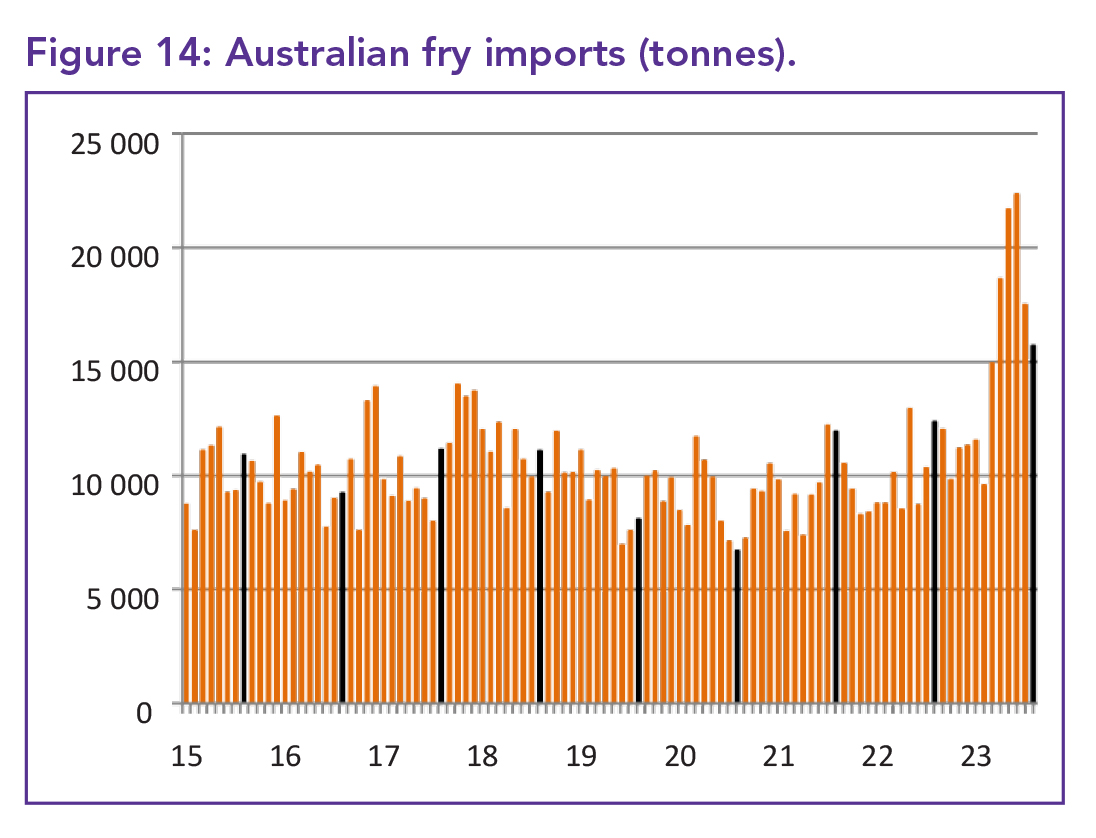

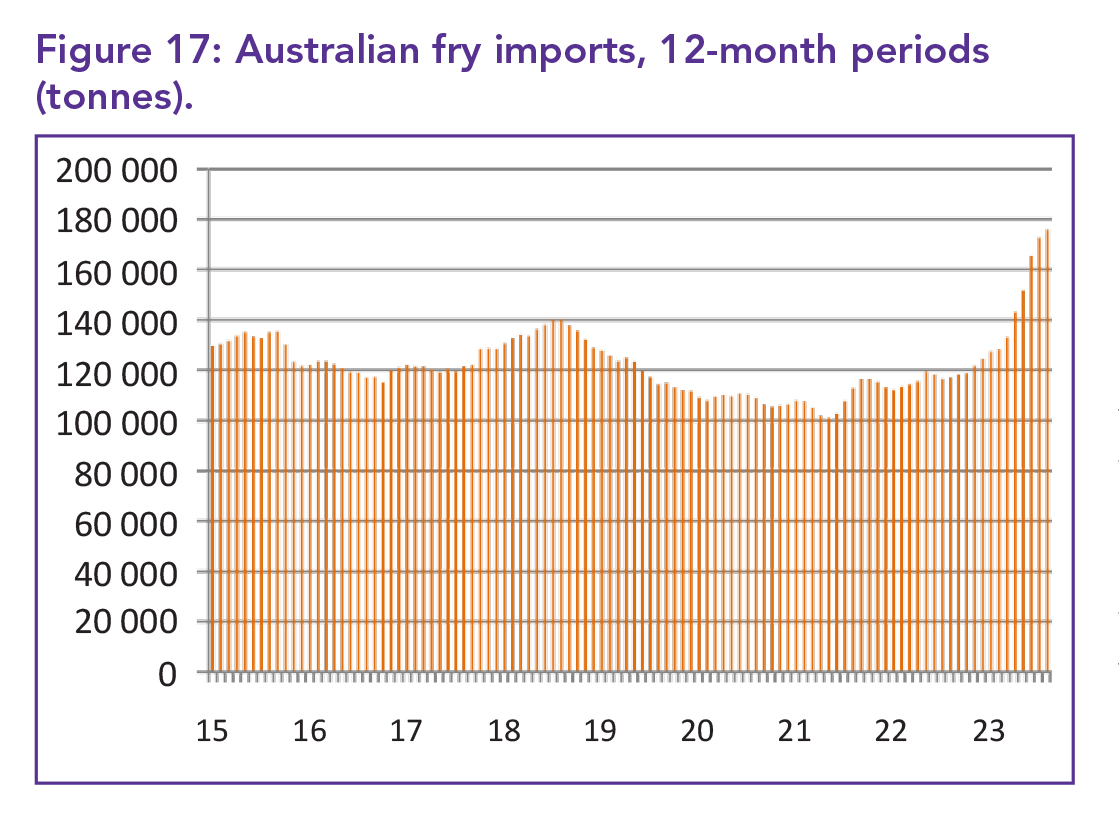

Frozen fry and other product imports in August hit a five-month low but remained 27% higher than in August 2022, totaling 15 692 tonnes. Annual imports reached a new all-time high of 176 044 tonnes, marking a 50.5% increase compared to 2021/22.

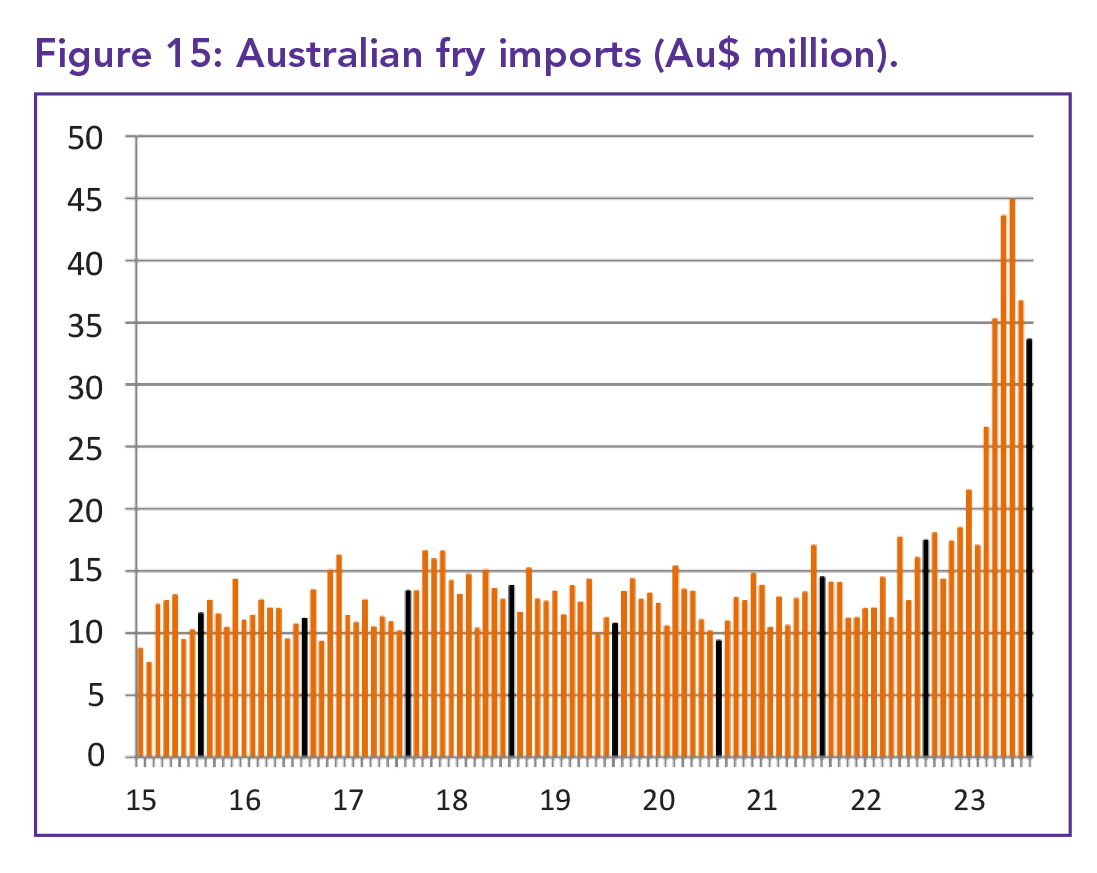

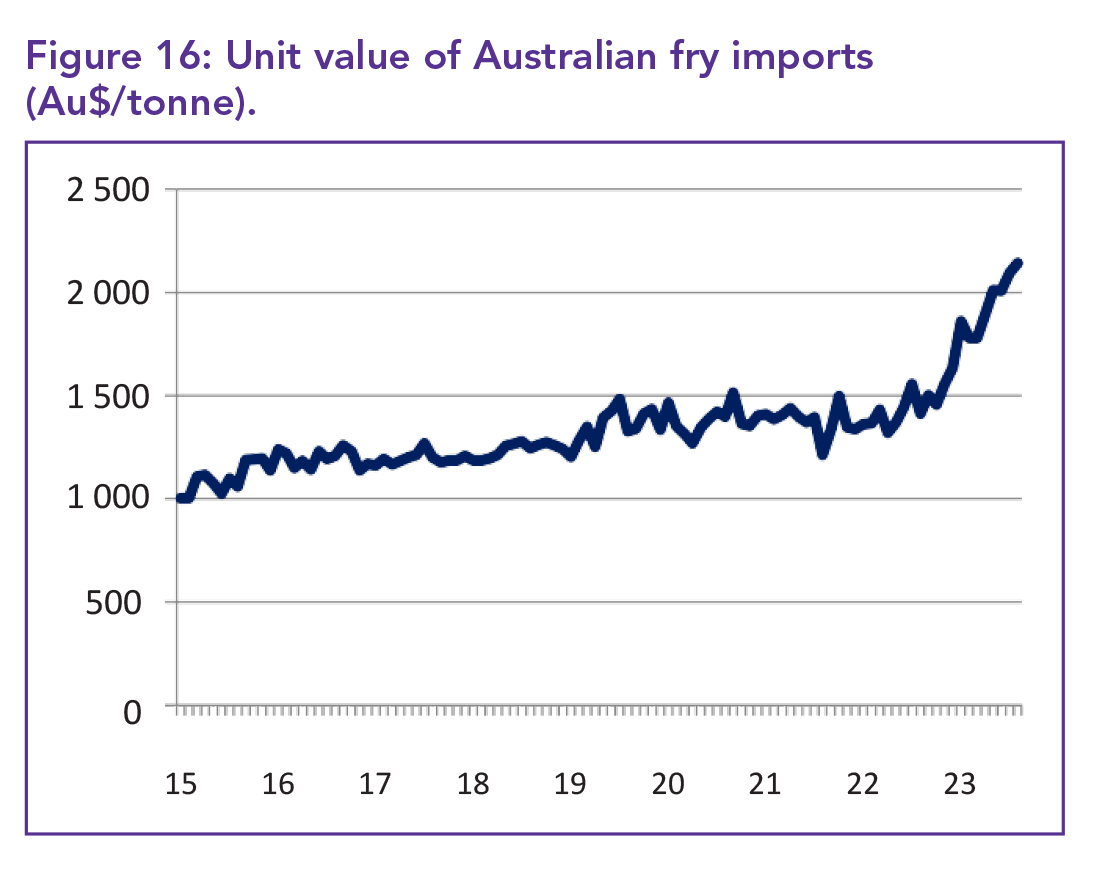

Despite the small quantity, importers were willing to pay exceptionally high prices for frozen fries, reaching a record price of Au$2 142/t (€1 434 or US$794) in August, representing a 51.6% increase from the same month in 2022. The total value of imports doubled in the year ending August 2023 to Au$329.059 million (€198.950 or US$209.750).

Belgium has significantly benefited from Australia’s demand for frozen potato products. Imports from Belgium doubled in August 2023 compared to August 2022, reaching 6 949 tonnes or 44% of the total.

Over the year, imports from Belgium surged by 133% to 68 249 tonnes, constituting 39% of the total. Despite not being a low-cost supplier, Belgian sales growth remained strong.

In August, the average price of Belgian fries was Au$2 315/tonne (€1 400 or US$1 476), marking a 42.5% increase from the previous year but 8.1% less than the average and 38% more than the lowest-priced supplier, France.

Dutch imports increased by 29.6% throughout the year and continued to rise in August. However, New Zealand imports, despite being among the lowest-priced products and covering a shorter distance, fell by 11.7% in the year ending August compared to the previous 12 months and 68.1% lower than in August 2022.

Smaller suppliers with modest bases experienced substantial increases, with French imports soaring by nearly 7 000% to 12 044 tonnes, while UK trade increased by almost 8 000% to 1 935 tonnes.

Due to a lack of domestic supplies resulting from challenging harvests, Australian exports continued to decline. In August 2023, only 823 tonnes were exported, representing a 23.7% decrease from August 2022, and annual exports were down 26.2% to 9 031 tonnes. The average price of exports increased by 15.7% to Au$2 372/t (€1 434 or US$1 512) between August 2022 and August 2023.

For more world potato market information, visit www.potatoes.co.za